Vastuuvelan riskimarginaalit. Aktuaariyhdistyksen vuosikokous Jukka Rantala

|

|

|

- Santeri Mäkelä

- 8 vuotta sitten

- Katselukertoja:

Transkriptio

1 Vastuuvelan riskimarginaalit Aktuaariyhdistyksen vuosikokous Jukka Rantala

2 2 Sisältö Taustaa IASB:n näkemys vastuuvelasta IAIS:n näkemys vastuuvelasta IAA:n riskimarginaalityöryhmän raportin luonnos CEIOPS:n neuvot Riskimarginaali ja vakavaraisuusvaatimukset

3 3 Taustaa IASB:n vakuutussopimusprojekti - Fair value-pohjainen varojen ja velkojen arviointi IAIS:n pyrkimys luoda vakavaraisuusvalvonnalle kansainvälinen kehikko - laajalti huolta, että IASB:n projekti johtaisi lopulta vakuutusalan vakavaraisuusvalvonnan tilanteen heikkenemiseen IAA - pelko siitä, ettei IASB riittävästi ymmärrä vakuutustoiminnan erityispiirteitä ja joutuu siten haitallisille harhapoluille Lausunnot IASB vakuutusprojektiin + standardit, Solvenssikirja halu välttää kaksia vastuuvelan laskentatapoja - yrittää vaikuttaa yhdessä IAIS:n kanssa Yhteisiä työryhmiä IAIS:n kanssa, IAIS:n Insurance Contracts ja Solvency alakomiteat, IAA:n Regulation ja Accounting komiteat, Risk Margin WG

4 4 IASB:n alustavat johtopäätökset In measuring its insurance liabilities, an insurer should use the following three building blocks: - current unbiased probability-weighted estimates of future cash flows - current market discount rates that adjust the estimated future cash flows for the time value of money - an explicit and unbiased estimate of the margin that market participants require for bearing risk (a risk margin) and for providing other services, if any (a service margin)

5 To the extent possible, current estimates should be consistent with observed market prices 5 Some estimates relate to observable market variables, such as interest rates. An insurer should use these variables as direct inputs without adjustment. Other estimates relate to variables (such as mortality) that cannot, in general, be observed directly from market prices and transactions. These estimates should be reviewed every year and updated if they are no longer consistent with all available information about current conditions should not contradict observable market variables should not incorporate the effect of synergies with other assets and liabilities. For example, if an insurer is significantly more or less efficient than other market participants, its estimates of cash flows should not reflect its own efficiencies or inefficiencies

6 6 Discount rates should be consistent with observable market prices for cash flows whose characteristics match those of the insurance liability. Those characteristics include timing, currency and liquidity. exclude any factors that influence observed interest rates but are not relevant to the liability (for example, risks that affect the observed rate but are not present in the liability).

7 7 Estimating the margin Vähemmistö: an insurer should calibrate the margin at inception to the price observed in the transaction with the policyholder: thus an insurer would not recognise a net gain at inception Enemmistö: an unbiased estimate of the margin another party would require if it took over the insurer s contractual rights and obligations The Board does not intend to prescribe specific methods for determining margins, but does intend to give some guidance on characteristics that a margin would need to have Some other initiatives may lead to useful inputs for guidance on risk margins - IAA Risk Margin Working Group - Several supervisors have been developing ideas on risk margins for solvency, for example in the European Solvency 2 project - Several insurers have been developing thoughts on risk margins for solvency and for internal economical capital projects

8 8 Service margin Many insurance contracts require an insurer to provide services in addition to the service of bearing risk the measurement of an insurance liability should include a service margin if market participants typically require such a margin. This has the following implications - If the contract explicitly or implicitly provides the fee that market participants typically require, the insurer recognises an asset and measures it at the amount of the origination costs that market participants typically incur - If market participants typically require a higher explicit or implicit service fee, the initial measurement of the asset is less than the origination costs that market participants typically incur - When the insurer renders the related service in later periods, it releases the service margin and recognises revenue. The revenue is the margin that market participants would require, not the margin that is implicit or explicit in the contract. - If it becomes clear during the life of that contract that market participants would require a higher service margin than previously estimated, the measurement of the liability increases.

9 9 Service margin (IAA RMWG) Service margin represents the compensation required to provide such services, such as investment management services, as long as market participants typically require such a margin. Its objective is to avoid the front-ending of this expected future margin on such services as profit. This margin is conceptually similar to the risk margin. It reflects the difference between the total price charged by a market participant for the obligation to provide such services and the already considered current estimate and risk margin. It is especially important in view of the long term nature of many insurance contracts, as insurers often promise administrative services to policyholders for a long period of time, often at a fixed price.

10 10 IAIS:n dokumentit A new framework for insurance supervision: Towards a common structure and common standards for the assessment of insurance solvency, October 2005 Towards a common structure and common standards for the assessment of insurer solvency: cornerstones for the formulation of regulatory financial requirements, October 2005 Issues arising as a result of the IASB s Insurance Contracts Project Phase II, Second Set of IAIS Observations, May 2006 The IAIS Common Structure for the assessment of insurer solvency, Draft 23 January 2007

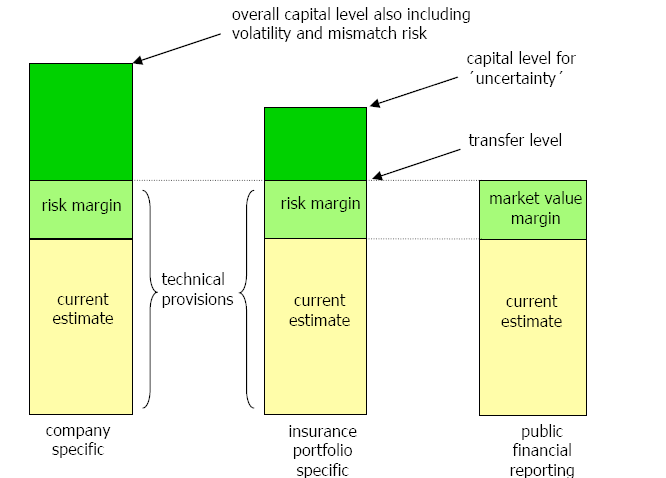

11 11 IAIS:n keskeisiä kannanottoja Total Balance Sheet lähestymistapa vakavaraisuusvalvontaan Tavoitteena tulisi olla saman vastuuvelan käyttö valvonta- ja talousraportointitarkoituksiin niin pitkälti kuin mahdollista Valvonnan kannalta vakavaraisuuspääoman tarkoitus on varmistaa, että korvaukset pystytään maksamaan ja vastuut kattamaan ajallaan ja suurella todennäköisyydellä Markkinadataa käytetään aina kun sitä olemassa ja loppu mallinnetaan markkinoita matkien Vastuun arvioinnin periaate pitäisi mieluummin lähteä vakuutussopimusten normaalista päättämisestä kuin oletuksesta kannansiirrosta; ts. pohjana ovat kassavirrat, jotka perustuvat vakuutussopimuksen mukaisiin suorituksiin edunsaajille Vastuuvelkaan on sisällyttävä riskimarginaali, joka pitäisi mitoittaa niin, että vastuuvelka vastaisi määrää, jonka kannan vastaanottavan vakuutusyhtiön voi vastuunsiirrossa odottaa vaativan vastaanottamiensa velvoitteiden kattamiseen

12 IAIS:n keskeisiä kannanottoja 12 A market consistent valuation of technical provisions should be based on the risk characteristics of the portfolio rather than the characteristics of the specific insurer holding the portfolio. - However it may be appropriate to use assumptions that reflect aspects of the insurer s specific business model and practices where they can be sufficiently substantiated. In a market consistent valuation methodology, technical provisions should be calibrated based on assumptions about diversification of the relevant risk factors which are consistent with market assumptions. Lack of diversification within a risk factor, relative to these assumptions, should be reflected in (increased) required capital, not in technical provisions. Mismatch risk exposure which is not intrinsic to the policy portfolio and is assumed voluntarily by the insurer should be reflected in required capital, and not in the technical provisions. the solvency regime requires the determination of a best estimate of the costs of meeting the obligations arising from the insurance portfolio, taking into account the time value of money, determined by reference to the relevant risk-free interest rates on the financial markets

13 IAIS:n vaatimuksia riskimarginaalin ominaisuuksille 13 Epävarmoissa kassavirroissa arviointi perustuu todennäköisyyksiin Exit model on suositeltava, mutta voittoa saisi sopimuksenteon hetkellä näyttää vain, jos vastuuvelan riskimarginaali on appropriate and sufficiently reliable Samanlaisten velvoitteiden ja riskien tulisi johtaa samanlaiseen vastuuseen Eivät preferoi tässä vaiheessa mitään riskimarginaalin laskentatapaa muiden edelle, mutta tuloksena olevan riskimarginaalin tulisi täyttää tiettyjä ominaisuuksia

14 IAIS:n vaatimuksia riskimarginaalin ominaisuuksille 14 Tulisi edistää läpinäkyvyyttä ja verrattavuutta Vakuutuksenottajan käyttäytyminen otettava huomioon ja tällöin tarkasteltava vakuutussopimusta kokonaisuutena ei yksittäisten piirteiden kannalta Ei ole tarvetta asettaa vastuuvelan minimiarvoksi takaisinostoarvoa Tulevat maksut tulee ottaa huomioon, jos ne liittyvät kiinteästi vakuutussopimuksen mukaisten velvoitteiden täyttämiseen Kassavirrat tulisi netottaa Ei hankintakulujen aktivointia, mutta hankintakuluja kattamaan tarkoitetut tulevat tuloerät voidaan ottaa huomioon Ehdollinen voitonjako osaksi vastuuvelkaa Johdannaiset sisällytettävä Oma luottoluokitus ei saa vaikuttaa

15 15

16 16 IAA:n Risk Margin Working group, draft report This report was prepared by the Risk Margin Working Group ( RMWG ) of the International Actuarial Association ( IAA ) in a response to a request of the Solvency and Actuarial Issues Subcommittee and Insurance Contracts Committee of the International Association of Insurance Supervisors. The RMWG has adopted the use of the term current estimate and margin over current estimate as standard terminology, although the latter is also referred to here as a "risk margin." Note that, in other literature, the current estimate phrase sometimes includes both concepts (i.e., the combination of the current estimate and the margin over current estimate as used in this report).

17 17 Riskien huomioonotto vastuuvelassa ja pääomavaatimuksessa vv ja pääoma vain pääoma Underwriting (insurance risk) x Underwriting (service risk) x Credit risk (that can be replicated) x Credit risk (that cannot be replicated) x Market risk (that can be replicated) x Market risk (that cannot be replicated) x Operational risk x Current (best) estimate x Current estimate uncertainty x Current estimate volatility x Catastrophe (very long tail) risk x Risk mitigation techniques x Risk concentration x Product adjustability features x Time risks over their life x Time ruin over short period x

18 18 RMWG:n pohdintaa valvonnan ja yleisen talousraportoinnin marginaalien eroista In the general purpose financial reporting sense, the amount incorporated in the insurance liability for current estimate uncertainty under an exit value approach for any risk is the amount that would be required to compensate a transferee for the risk inherent in a transfer of the net obligations, bearing in mind what is known of the probability distributions of the insured risk. In the regulatory sense, the emphasis is less on the expected market price, and more on the level of confidence which the current estimate and the risk margin in the liability together with the required capital provides for the overall sufficiency of the solvency assessment regime. In both cases, one of the key characteristics of the risk margin is to reflect the uncertainty in the calculation of the current estimate.

19 19 Desirable risk margin characteristics The less that is known about the current estimate and its trend; the higher the risk margins should be Risks with low frequency and high severity will have higher risk margins than risks with high frequency and low severity For similar risks, contracts that persist over a longer timeframe will have higher risk margins than those of shorter duration Risks with a wide probability distribution will have higher risk margins than those risks with a narrower distribution To the extent that emerging experience reduces uncertainty, risk margins will decrease, and vice versa. While the characteristics are expressed in a form that is risk oriented, the RMWG believes that the characteristics are also expressed reflecting the way the insurer to insurer (exit value) market works in practice where such markets exist. Given two well informed willing parties, the price demanded (and accepted) for risk transfer would incorporate these characteristics.

20 20 Desirable risk margin characteristics The risk margin methodology should have a consistent basis at issue and subsequent to issue, i.e., for the entire lifetime of the contract Use underlying assumptions consistent with those used in the determination of the corresponding current estimates Have a consistent risk margin methodology with other financial contracts; and Where possible, be determined in a manner consistent with accepted economic and actuarial pricing methodologies. The risk uncertainty itself should reflect knowledge about the risk(s) assumed, including observable information concerning the uncertainty associated with: - the estimated current level of the risk(s); - the estimated future level or trend of the risk(s), as applicable; - the estimated future term of the risk(s); and - the estimated future uncertainty associated with the first three sets of risk

21 21 Riskimarginaalin määräämistapoja Explicit assumption approaches. These risk margin methods use appropriate margins for adverse deviation on top of realistic current estimate assumptions. - Voi tulla kyseeseen, jos on olemassa erityisiä rajoituksia kuten ei voitonnäyttöä vakuutuksen alkaessa Quantile methods. These risk margin methods express uncertainty in terms of the excess of a percentile (quantile) for a given confidence level above the expected value for a given period, such as the lifetime of the coverage. - (e.g., confidence, CTE or moments) Cost of capital methods. These risk margin methods are determined based on the cost of holding the capital needed to perform the obligation. - This method appears to meet the IASB s primary objective of reflecting market charges for assuming risk, as well as that of the IAIS.

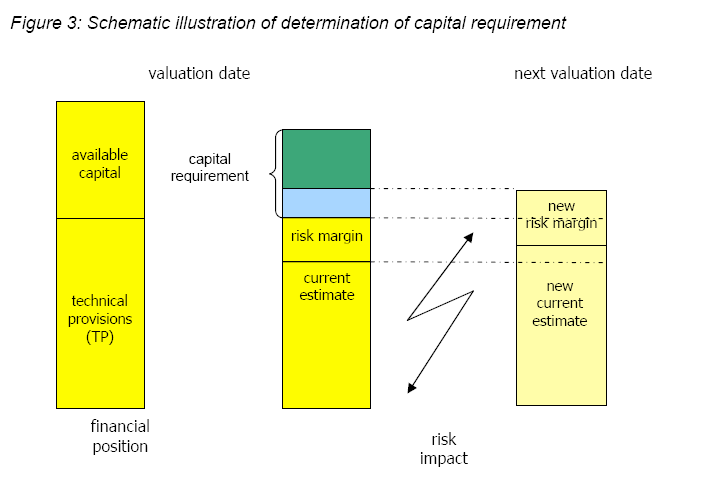

22 22 Cost of capital method The cost of capital method is based on the explicit assumption that, at each point in time, the risk margin must be sufficient to finance the (solvency) capital. Otherwise a transferee will be unwilling to pay less than an amount that would fund future capital requirements. Reflection of the estimated current and future economic capital needs of a potential transferee ensures that the amount paid for the transferee for risk provides for the entire risk that will affect the purchaser. Implementing the cost of capital method requires determination of the cost of capital from the perspective of the transferee. The cost of capital for this purpose is the before-the-event target intended to produce a desired after-the-event pre-tax return on the capital

23 23 Cost of capital metodissa tarvittavia oletuksia Reference entity - the entity to which the capital should relate: consistent with an exit value approach, it is reasonable to construct a reference entity to which the portfolio would be transferred Capital Capital release over time - The assumption that future capital needs is a constant percentage of the current estimate or the risk margin may not be appropriate. Cost of capital - In discussions of the cost of capital method, 4% and 6% have typically been used to illustrate the method. 6% is used in the example provided in the Swiss Solvency Test described as the cost of capital associated with a BBB company

24 24 Risk margin results for P/C insurance Longer tail, Risk free rate =4%, Cost of capital method Assumptions Capital % Capital % Cost of Increase 10 % per Capital Constant year Constant Initial Capital % Longer Tail Medium Tail Increase 10 % per year 30.0% 4.0% 6.1% 8.5% 2.2% 2.3% 30.0% 6.0% 8.8% 12.7% 3.2% 3.5% 30.0% 10.0% 14.7% 21.2% 5.4% 5.8% 60.0% 4.0% 11.8% 17.0% 4.3% 4.6% 60.0% 6.0% 17.7% 25.5% 6.5% 7.0% 60.0% 10.0% 29.4% 42.5% 10.8% 11.6%

25 Implied discount rate Medium tail, Risk free rate =4%, Cost of capital method 25 Assumptions Capital % Capital % Cost of Increase 10 % per Capital Constant year Constant Initial Capital % Longer Tail Medium Tail Increase 10 % per year 30.0% 4.0% -4.1% 2.4% 2.8% 2.7% 30.0% 6.0% -2.1% 1.7% 2.3% 2.1% 30.0% 10.0% 0.0% 0.3% 1.1% 1.0% 60.0% 4.0% -1.1% 1.0% 1.7% 1.5% 60.0% 6.0% 2.9% -0.3% 0.6% 0.4% 60.0% 10.0% 0.0% -2.6% -1.5% -1.9%

26 26 Translation of cost of capital method into quantile method cost of capital based on a 99.5% capital and a 4% cost Normal Typical Long-Tail Extreme Short term #sigma Gamma Quantile 59% 63% 67% 84% Medium term #sigma Gamma Quantile 73% 77% 81% 91% Long term #sigma Gamma Quantile 79% 83% 86% 94%

27 Risk margin comparison -- single premium annuity Margin Year CoC Quantile approach

28 Risk margin comparisons with consistent initial values single premium annuity Risk margin comparison Margin CoC Year Quantile approach

29 29 CEIOPS' Advice Role of technical provisions and capital requirements Reflecting existing market uncertainties the cost of capital must consist of a conservative market value margin that meets the objectives either: To transfer the liabilities portfolio to an able, rational and willing thirdparty (another (re)insurer) with a sufficiently high level of confidence; or To recapitalize the company with a sufficiently high level of confidence to ensure a proper run-off scenario by the original undertaking. Both technical provisions and capital requirements are part of a consistent overall framework, which aims to ensure an adequate level of protection of policyholders and beneficiaries: Technical provisions represent the amount that is required for an insurer to settle all insurance liabilities to policyholders and other beneficiaries arising over the lifetime of the portfolio; Capital provides further safeguarding of the policyholders and beneficiaries by 'protecting' the technical provisions and the assets backing them. - As to the calculation of the risk margin, the cost of capital approach should be used under certain preconditions to be defined in the Framework Directive, using historical volatilities in credit spreads for a BBB rating (corresponding to a 99,5 % confidence level).

30 30 Riskimarginaali ja solvenssi Riskimarginaalin määrääminen on kallistumassa siihen, että sen laskennassa oletetaan kannansiirto Onko solvenssivaatimuksessa otettava huomioon mahdollisuus, ettei kannansiirto onnistu? Silloin solvenssivaatimuksen tulisi perustua kvantiilimetodiin

31 31

32 32 Vastuuvelka valvonnassa ja verotuksessa; yksi vaihtoehto Minimisolvenssivaatimus MCR/SCR perustuu vaatimukseen, että varat riittävät suurella todennäköisyydellä kattamaan mm. seuraavat riskit - Varoihin liittyvät riskit - Vastuuvelka, joka syntyy seuraavan vuoden uudesta ja uudistetusta liikkeestä ottaen huomioon niihin liittyvä maksutulo - Vanhan vastuuvelan riski, joka koostuu ennakoitujen ja toteutuvien kassavirojen erotukseen ja seuraavan vuoden lopun ja vuoden alun vastuuvelkojen erotukseen Vanhaa vastuuvelkaa koskevat säännökset (katesäännökset, etuoikeussäännökset, verosäännökset) voitaisiin ulottaa koskemaan MCR/SCR:ää

33 33 Groupen lausunto CP 20:een We accept that it might be reasonable to require that the change to Solvency II should not give rise to a reduction in the total (technical provisions plus SCR) for a transitional period, which however should be short. One of the impacts of displacement of prudence from technical provisions to capital could be: A prudential calculation of technical provisions may suggest a better protection to policyholders than the MCR, because technical provisions are usually in many ways ring fenced (e.g. by priority rules in case of bankruptcy, by rules for assets backing the provisions, maybe taxation) to policyholders, whereas the solvency capital is not. Those ring fencing rules should be reviewed in order to judge if they should be extended to cover technical provisions and the SCR.

Vastuuvelan markkina-arvon määrittämisestä *

Vastuuvelan markkina-arvon määrittämisestä * 13.10.2008 Markku Miettinen * Market Value of Liabilities for Insurance Firms, CRO Forum, July 2008 1 Eri lähestymistapoja / periaatteita vastuuvelan parhaan

Vastuuvelan markkina-arvon määrittämisestä * 13.10.2008 Markku Miettinen * Market Value of Liabilities for Insurance Firms, CRO Forum, July 2008 1 Eri lähestymistapoja / periaatteita vastuuvelan parhaan

Capacity Utilization

Capacity Utilization Tim Schöneberg 28th November Agenda Introduction Fixed and variable input ressources Technical capacity utilization Price based capacity utilization measure Long run and short run

Capacity Utilization Tim Schöneberg 28th November Agenda Introduction Fixed and variable input ressources Technical capacity utilization Price based capacity utilization measure Long run and short run

Efficiency change over time

Efficiency change over time Heikki Tikanmäki Optimointiopin seminaari 14.11.2007 Contents Introduction (11.1) Window analysis (11.2) Example, application, analysis Malmquist index (11.3) Dealing with panel

Efficiency change over time Heikki Tikanmäki Optimointiopin seminaari 14.11.2007 Contents Introduction (11.1) Window analysis (11.2) Example, application, analysis Malmquist index (11.3) Dealing with panel

Network to Get Work. Tehtäviä opiskelijoille Assignments for students. www.laurea.fi

Network to Get Work Tehtäviä opiskelijoille Assignments for students www.laurea.fi Ohje henkilöstölle Instructions for Staff Seuraavassa on esitetty joukko tehtäviä, joista voit valita opiskelijaryhmällesi

Network to Get Work Tehtäviä opiskelijoille Assignments for students www.laurea.fi Ohje henkilöstölle Instructions for Staff Seuraavassa on esitetty joukko tehtäviä, joista voit valita opiskelijaryhmällesi

16. Allocation Models

16. Allocation Models Juha Saloheimo 17.1.27 S steemianalsin Optimointiopin seminaari - Sks 27 Content Introduction Overall Efficienc with common prices and costs Cost Efficienc S steemianalsin Revenue

16. Allocation Models Juha Saloheimo 17.1.27 S steemianalsin Optimointiopin seminaari - Sks 27 Content Introduction Overall Efficienc with common prices and costs Cost Efficienc S steemianalsin Revenue

LUONNOS RT 80260 EN AGREEMENT ON BUILDING WORKS 1 THE PARTIES. May 1998 1 (10)

") RT 80260 EN May 1998 1 (10) AGREEMENT ON BUILDING WORKS This agreement template is based on the General Terms and Conditions of Building Contracts YSE 1998 RT 16-10660, LVI 03-10277, Ratu 417-7, KH X4-00241.

RT 80260 EN May 1998 1 (10) AGREEMENT ON BUILDING WORKS This agreement template is based on the General Terms and Conditions of Building Contracts YSE 1998 RT 16-10660, LVI 03-10277, Ratu 417-7, KH X4-00241.

Other approaches to restrict multipliers

Other approaches to restrict multipliers Heikki Tikanmäki Optimointiopin seminaari 10.10.2007 Contents Short revision (6.2) Another Assurance Region Model (6.3) Cone-Ratio Method (6.4) An Application of

Other approaches to restrict multipliers Heikki Tikanmäki Optimointiopin seminaari 10.10.2007 Contents Short revision (6.2) Another Assurance Region Model (6.3) Cone-Ratio Method (6.4) An Application of

The CCR Model and Production Correspondence

The CCR Model and Production Correspondence Tim Schöneberg The 19th of September Agenda Introduction Definitions Production Possiblity Set CCR Model and the Dual Problem Input excesses and output shortfalls

The CCR Model and Production Correspondence Tim Schöneberg The 19th of September Agenda Introduction Definitions Production Possiblity Set CCR Model and the Dual Problem Input excesses and output shortfalls

IAA Regulation Committee

IAA Regulation Committee Mikä IRC on? Insurance Regulation Committee Insurance Regulation Committee ORSA Working Group Insurance Regulation Committee Reinsurance Insurance Regulation Committee Solvency

IAA Regulation Committee Mikä IRC on? Insurance Regulation Committee Insurance Regulation Committee ORSA Working Group Insurance Regulation Committee Reinsurance Insurance Regulation Committee Solvency

On instrument costs in decentralized macroeconomic decision making (Helsingin Kauppakorkeakoulun julkaisuja ; D-31)

") On instrument costs in decentralized macroeconomic decision making (Helsingin Kauppakorkeakoulun julkaisuja ; D-31) Juha Kahkonen Click here if your download doesn"t start automatically On instrument costs

On instrument costs in decentralized macroeconomic decision making (Helsingin Kauppakorkeakoulun julkaisuja ; D-31) Juha Kahkonen Click here if your download doesn"t start automatically On instrument costs

Valuation of Asian Quanto- Basket Options

Valuation of Asian Quanto- Basket Options (Final Presentation) 21.11.2011 Thesis Instructor and Supervisor: Prof. Ahti Salo Työn saa tallentaa ja julkistaa Aalto-yliopiston avoimilla verkkosivuilla. Muilta

Valuation of Asian Quanto- Basket Options (Final Presentation) 21.11.2011 Thesis Instructor and Supervisor: Prof. Ahti Salo Työn saa tallentaa ja julkistaa Aalto-yliopiston avoimilla verkkosivuilla. Muilta

Työsuojelurahaston Tutkimus tutuksi - PalveluPulssi 11.3.2016. Peter Michelsson Wallstreet Asset Management Oy

Työsuojelurahaston Tutkimus tutuksi - PalveluPulssi 11.3.2016 Peter Michelsson Wallstreet Asset Management Oy Wallstreet lyhyesti Perustettu vuonna 2006, SiPa toimilupa myönnetty 3/2014 Täysin kotimainen,

Työsuojelurahaston Tutkimus tutuksi - PalveluPulssi 11.3.2016 Peter Michelsson Wallstreet Asset Management Oy Wallstreet lyhyesti Perustettu vuonna 2006, SiPa toimilupa myönnetty 3/2014 Täysin kotimainen,

AYYE 9/ HOUSING POLICY

AYYE 9/12 2.10.2012 HOUSING POLICY Mission for AYY Housing? What do we want to achieve by renting apartments? 1) How many apartments do we need? 2) What kind of apartments do we need? 3) To whom do we

AYYE 9/12 2.10.2012 HOUSING POLICY Mission for AYY Housing? What do we want to achieve by renting apartments? 1) How many apartments do we need? 2) What kind of apartments do we need? 3) To whom do we

Alternative DEA Models

Mat-2.4142 Alternative DEA Models 19.9.2007 Table of Contents Banker-Charnes-Cooper Model Additive Model Example Data Home assignment BCC Model (Banker-Charnes-Cooper) production frontiers spanned by convex

Mat-2.4142 Alternative DEA Models 19.9.2007 Table of Contents Banker-Charnes-Cooper Model Additive Model Example Data Home assignment BCC Model (Banker-Charnes-Cooper) production frontiers spanned by convex

On instrument costs in decentralized macroeconomic decision making (Helsingin Kauppakorkeakoulun julkaisuja ; D-31)

") On instrument costs in decentralized macroeconomic decision making (Helsingin Kauppakorkeakoulun julkaisuja ; D-31) Juha Kahkonen Click here if your download doesn"t start automatically On instrument costs

On instrument costs in decentralized macroeconomic decision making (Helsingin Kauppakorkeakoulun julkaisuja ; D-31) Juha Kahkonen Click here if your download doesn"t start automatically On instrument costs

Markku Paakkanen IAS-katsaus. IASB:n kannanottoja vaiheen 1 standardiluonnoskommentteihin IAA:n laskenta- ja aktuaaristandardikomiteoiden

IASB:n kannanottoja vaiheen 1 standardiluonnoskommentteihin IAA:n laskenta- ja aktuaaristandardikomiteoiden kannanottoja Vaihe I Vakuutusvastuiden katteena oleva varat Väliaikainen poikkeuslupa IAS-raamista

IASB:n kannanottoja vaiheen 1 standardiluonnoskommentteihin IAA:n laskenta- ja aktuaaristandardikomiteoiden kannanottoja Vaihe I Vakuutusvastuiden katteena oleva varat Väliaikainen poikkeuslupa IAS-raamista

Statistical design. Tuomas Selander

Statistical design Tuomas Selander 28.8.2014 Introduction Biostatistician Work area KYS-erva KYS, Jyväskylä, Joensuu, Mikkeli, Savonlinna Work tasks Statistical methods, selection and quiding Data analysis

Statistical design Tuomas Selander 28.8.2014 Introduction Biostatistician Work area KYS-erva KYS, Jyväskylä, Joensuu, Mikkeli, Savonlinna Work tasks Statistical methods, selection and quiding Data analysis

Infrastruktuurin asemoituminen kansalliseen ja kansainväliseen kenttään Outi Ala-Honkola Tiedeasiantuntija

Infrastruktuurin asemoituminen kansalliseen ja kansainväliseen kenttään Outi Ala-Honkola Tiedeasiantuntija 1 Asemoitumisen kuvaus Hakemukset parantuneet viime vuodesta, mutta paneeli toivoi edelleen asemoitumisen

Infrastruktuurin asemoituminen kansalliseen ja kansainväliseen kenttään Outi Ala-Honkola Tiedeasiantuntija 1 Asemoitumisen kuvaus Hakemukset parantuneet viime vuodesta, mutta paneeli toivoi edelleen asemoitumisen

Karkaavatko ylläpitokustannukset miten kustannukset ja tuotot johdetaan hallitusti?

For professional use only Not for public distribution Karkaavatko ylläpitokustannukset miten kustannukset ja tuotot johdetaan hallitusti? 08.02.2012 Jyrki Merjamaa, Head of Asset Management Aberdeen Asset

For professional use only Not for public distribution Karkaavatko ylläpitokustannukset miten kustannukset ja tuotot johdetaan hallitusti? 08.02.2012 Jyrki Merjamaa, Head of Asset Management Aberdeen Asset

EUROOPAN PARLAMENTTI

EUROOPAN PARLAMENTTI 2004 2009 Kansalaisvapauksien sekä oikeus- ja sisäasioiden valiokunta 2008/0101(CNS) 2.9.2008 TARKISTUKSET 9-12 Mietintöluonnos Luca Romagnoli (PE409.790v01-00) ehdotuksesta neuvoston

EUROOPAN PARLAMENTTI 2004 2009 Kansalaisvapauksien sekä oikeus- ja sisäasioiden valiokunta 2008/0101(CNS) 2.9.2008 TARKISTUKSET 9-12 Mietintöluonnos Luca Romagnoli (PE409.790v01-00) ehdotuksesta neuvoston

1. SIT. The handler and dog stop with the dog sitting at heel. When the dog is sitting, the handler cues the dog to heel forward.

START START SIT 1. SIT. The handler and dog stop with the dog sitting at heel. When the dog is sitting, the handler cues the dog to heel forward. This is a static exercise. SIT STAND 2. SIT STAND. The

START START SIT 1. SIT. The handler and dog stop with the dog sitting at heel. When the dog is sitting, the handler cues the dog to heel forward. This is a static exercise. SIT STAND 2. SIT STAND. The

Innovative and responsible public procurement Urban Agenda kumppanuusryhmä. public-procurement

Innovative and responsible public procurement Urban Agenda kumppanuusryhmä https://ec.europa.eu/futurium/en/ public-procurement Julkiset hankinnat liittyvät moneen Konsortio Lähtökohdat ja tavoitteet Every

Innovative and responsible public procurement Urban Agenda kumppanuusryhmä https://ec.europa.eu/futurium/en/ public-procurement Julkiset hankinnat liittyvät moneen Konsortio Lähtökohdat ja tavoitteet Every

Tarua vai totta: sähkön vähittäismarkkina ei toimi? 11.2.2015 Satu Viljainen Professori, sähkömarkkinat

Tarua vai totta: sähkön vähittäismarkkina ei toimi? 11.2.2015 Satu Viljainen Professori, sähkömarkkinat Esityksen sisältö: 1. EU:n energiapolitiikka on se, joka ei toimi 2. Mihin perustuu väite, etteivät

Tarua vai totta: sähkön vähittäismarkkina ei toimi? 11.2.2015 Satu Viljainen Professori, sähkömarkkinat Esityksen sisältö: 1. EU:n energiapolitiikka on se, joka ei toimi 2. Mihin perustuu väite, etteivät

Information on preparing Presentation

Information on preparing Presentation Seminar on big data management Lecturer: Spring 2017 20.1.2017 1 Agenda Hints and tips on giving a good presentation Watch two videos and discussion 22.1.2017 2 Goals

Information on preparing Presentation Seminar on big data management Lecturer: Spring 2017 20.1.2017 1 Agenda Hints and tips on giving a good presentation Watch two videos and discussion 22.1.2017 2 Goals

Rotarypiiri 1420 Piiriapurahoista myönnettävät stipendit

Rotarypiiri 1420 Piiriapurahoista myönnettävät stipendit Ø Rotarypiiri myöntää stipendejä sille osoitettujen hakemusten perusteella ensisijaisesti rotaryaatteen mukaisiin tarkoituksiin. Ø Stipendejä myönnetään

Rotarypiiri 1420 Piiriapurahoista myönnettävät stipendit Ø Rotarypiiri myöntää stipendejä sille osoitettujen hakemusten perusteella ensisijaisesti rotaryaatteen mukaisiin tarkoituksiin. Ø Stipendejä myönnetään

Olet vastuussa osaamisestasi

Olet vastuussa osaamisestasi Ohjelmistoammattilaisuuden uudet haasteet Timo Vehmaro 02-12-2015 1 Nokia 2015 Mitä osaamista tulevaisuudessa tarvitaan? Vahva perusosaaminen on kaiken perusta Implementaatio

Olet vastuussa osaamisestasi Ohjelmistoammattilaisuuden uudet haasteet Timo Vehmaro 02-12-2015 1 Nokia 2015 Mitä osaamista tulevaisuudessa tarvitaan? Vahva perusosaaminen on kaiken perusta Implementaatio

LX 70. Ominaisuuksien mittaustulokset 1-kerroksinen 2-kerroksinen. Fyysiset ominaisuudet, nimellisarvot. Kalvon ominaisuudet

LX 70 % Läpäisy 36 32 % Absorptio 30 40 % Heijastus 34 28 % Läpäisy 72 65 % Heijastus ulkopuoli 9 16 % Heijastus sisäpuoli 9 13 Emissiivisyys.77.77 Auringonsuojakerroin.54.58 Auringonsäteilyn lämmönsiirtokerroin.47.50

LX 70 % Läpäisy 36 32 % Absorptio 30 40 % Heijastus 34 28 % Läpäisy 72 65 % Heijastus ulkopuoli 9 16 % Heijastus sisäpuoli 9 13 Emissiivisyys.77.77 Auringonsuojakerroin.54.58 Auringonsäteilyn lämmönsiirtokerroin.47.50

Kaivostoiminnan eri vaiheiden kumulatiivisten vaikutusten huomioimisen kehittäminen suomalaisessa luonnonsuojelulainsäädännössä

M a t t i K a t t a i n e n O T M 1 1. 0 9. 2 0 1 9 Kaivostoiminnan eri vaiheiden kumulatiivisten vaikutusten huomioimisen kehittäminen suomalaisessa luonnonsuojelulainsäädännössä Ympäristöoikeustieteen

M a t t i K a t t a i n e n O T M 1 1. 0 9. 2 0 1 9 Kaivostoiminnan eri vaiheiden kumulatiivisten vaikutusten huomioimisen kehittäminen suomalaisessa luonnonsuojelulainsäädännössä Ympäristöoikeustieteen

On instrument costs in decentralized macroeconomic decision making (Helsingin Kauppakorkeakoulun julkaisuja ; D-31)

") On instrument costs in decentralized macroeconomic decision making (Helsingin Kauppakorkeakoulun julkaisuja ; D-31) Juha Kahkonen Click here if your download doesn"t start automatically On instrument costs

On instrument costs in decentralized macroeconomic decision making (Helsingin Kauppakorkeakoulun julkaisuja ; D-31) Juha Kahkonen Click here if your download doesn"t start automatically On instrument costs

Väite Argument "Yhteiskunnan velvollisuus on tarjota virkistysalueita ja -palveluita." "Recreation sites and service

Olisiko vastaaja valmis maksamaan... Would the respondent be willing to pay for... Luonto-opastuksesta Nature guide services Autiotuvan käytöstä Use of wilderness huts Tulipaikan käytöstä (polttopuut,

Olisiko vastaaja valmis maksamaan... Would the respondent be willing to pay for... Luonto-opastuksesta Nature guide services Autiotuvan käytöstä Use of wilderness huts Tulipaikan käytöstä (polttopuut,

Results on the new polydrug use questions in the Finnish TDI data

Results on the new polydrug use questions in the Finnish TDI data Multi-drug use, polydrug use and problematic polydrug use Martta Forsell, Finnish Focal Point 28/09/2015 Martta Forsell 1 28/09/2015 Esityksen

Results on the new polydrug use questions in the Finnish TDI data Multi-drug use, polydrug use and problematic polydrug use Martta Forsell, Finnish Focal Point 28/09/2015 Martta Forsell 1 28/09/2015 Esityksen

Curriculum. Gym card

A new school year Curriculum Fast Track Final Grading Gym card TET A new school year Work Ethic Detention Own work Organisation and independence Wilma TMU Support Services Well-Being CURRICULUM FAST TRACK

A new school year Curriculum Fast Track Final Grading Gym card TET A new school year Work Ethic Detention Own work Organisation and independence Wilma TMU Support Services Well-Being CURRICULUM FAST TRACK

Capacity utilization

Mat-2.4142 Seminar on optimization Capacity utilization 12.12.2007 Contents Summary of chapter 14 Related DEA-solver models Illustrative examples Measure of technical capacity utilization Price-based measure

Mat-2.4142 Seminar on optimization Capacity utilization 12.12.2007 Contents Summary of chapter 14 Related DEA-solver models Illustrative examples Measure of technical capacity utilization Price-based measure

Mawson Resources Limited

www.mawsonresources.com SYYSKUU 2014 Disclaimer Some of the statements contained in the following material may be "forward-looking statements." All statements, other than statements of historical fact,

www.mawsonresources.com SYYSKUU 2014 Disclaimer Some of the statements contained in the following material may be "forward-looking statements." All statements, other than statements of historical fact,

Wärtsilä Corporation. Interim Report January-September 2003 Ole Johansson President & CEO. 29 October Wärtsilä

Wärtsilä Corporation Interim Report January-September 2003 Ole Johansson President & CEO 29 October 2003 Highlights of the reporting period Order intake of Power Divisions increased. Clear improvement

Wärtsilä Corporation Interim Report January-September 2003 Ole Johansson President & CEO 29 October 2003 Highlights of the reporting period Order intake of Power Divisions increased. Clear improvement

Miehittämätön meriliikenne

Rolls-Royce & Unmanned Shipping Ecosystem Miehittämätön meriliikenne Digimurros 2020+ 17.11. 2016 September 2016 2016 Rolls-Royce plc The 2016 information Rolls-Royce in this plc document is the property

Rolls-Royce & Unmanned Shipping Ecosystem Miehittämätön meriliikenne Digimurros 2020+ 17.11. 2016 September 2016 2016 Rolls-Royce plc The 2016 information Rolls-Royce in this plc document is the property

LYTH-CONS CONSISTENCY TRANSMITTER

LYTH-CONS CONSISTENCY TRANSMITTER LYTH-INSTRUMENT OY has generate new consistency transmitter with blade-system to meet high technical requirements in Pulp&Paper industries. Insurmountable advantages are

LYTH-CONS CONSISTENCY TRANSMITTER LYTH-INSTRUMENT OY has generate new consistency transmitter with blade-system to meet high technical requirements in Pulp&Paper industries. Insurmountable advantages are

Returns to Scale II. S ysteemianalyysin. Laboratorio. Esitelmä 8 Timo Salminen. Teknillinen korkeakoulu

Returns to Scale II Contents Most Productive Scale Size Further Considerations Relaxation of the Convexity Condition Useful Reminder Theorem 5.5 A DMU found to be efficient with a CCR model will also be

Returns to Scale II Contents Most Productive Scale Size Further Considerations Relaxation of the Convexity Condition Useful Reminder Theorem 5.5 A DMU found to be efficient with a CCR model will also be

Sisäiset mallit. Aktuaariyhdistyksen Solvenssi II seminaari Helsinki Camilla Eriksson

Sisäiset mallit Aktuaariyhdistyksen Solvenssi II seminaari Helsinki 18.5.2010 amilla Eriksson Sisäinen malli ja sen tarkoitus Mikä on sisäinen malli? Riskienhallintajärjestelmä jonka vakuutusyhtiö kehittää

Sisäiset mallit Aktuaariyhdistyksen Solvenssi II seminaari Helsinki 18.5.2010 amilla Eriksson Sisäinen malli ja sen tarkoitus Mikä on sisäinen malli? Riskienhallintajärjestelmä jonka vakuutusyhtiö kehittää

Tutkimusdata ja julkaiseminen Suomen Akatemian ja EU:n H2020 projekteissa

Tutkimusdata ja julkaiseminen Suomen Akatemian ja EU:n H2020 projekteissa Tutkimusasiamies Kaisa Männikkö Tutkimus- ja innovaatiopalvelut Suomen Akatemian projektit Suomen Akatemia kehottaa avoimeen tieteelliseen

Tutkimusdata ja julkaiseminen Suomen Akatemian ja EU:n H2020 projekteissa Tutkimusasiamies Kaisa Männikkö Tutkimus- ja innovaatiopalvelut Suomen Akatemian projektit Suomen Akatemia kehottaa avoimeen tieteelliseen

Vastaa kysymyksiin ympyröimällä oikea vastausvaihtoehto.

Oulun yliopisto, OyKKK Mirjam Lehenkari 724207A RAHOIUSPÄÄÖKSE entti 2 (1. uusinta) 4.4.2016 entti koostuu 15 monivalinta- tai oikein/väärin tehtävästä. Jokaiseen tehtävään on ainoastaan yksi oikea (tai

Oulun yliopisto, OyKKK Mirjam Lehenkari 724207A RAHOIUSPÄÄÖKSE entti 2 (1. uusinta) 4.4.2016 entti koostuu 15 monivalinta- tai oikein/väärin tehtävästä. Jokaiseen tehtävään on ainoastaan yksi oikea (tai

LUONNOS. KVS2016 tariffirakenne esimerkkejä. Neuvottelukunta

LUONNOS KVS2016 tariffirakenne esimerkkejä Neuvottelukunta 19.5.2014 2 Esityksen sisältö 1. Kantaverkkotariffi 2014 2. Edellisen neuvottelukunnan kokouksen 19.3 evästeet 3. Sähkön tuotannon tariffin nykyinen

LUONNOS KVS2016 tariffirakenne esimerkkejä Neuvottelukunta 19.5.2014 2 Esityksen sisältö 1. Kantaverkkotariffi 2014 2. Edellisen neuvottelukunnan kokouksen 19.3 evästeet 3. Sähkön tuotannon tariffin nykyinen

CASE POSTI: KEHITYKSEN KÄRJESSÄ TALOUDEN SUUNNITTELUSSA KETTERÄSTI PALA KERRALLAAN

POSTI GROUP CASE POSTI: KEHITYKSEN KÄRJESSÄ TALOUDEN SUUNNITTELUSSA KETTERÄSTI PALA KERRALLAAN TIINA KATTILAKOSKI POSTIN TALOUDEN SUUNNITTELU Mistä lähdettiin liikkeelle? Ennustaminen painottui vuosisuunnitteluun

POSTI GROUP CASE POSTI: KEHITYKSEN KÄRJESSÄ TALOUDEN SUUNNITTELUSSA KETTERÄSTI PALA KERRALLAAN TIINA KATTILAKOSKI POSTIN TALOUDEN SUUNNITTELU Mistä lähdettiin liikkeelle? Ennustaminen painottui vuosisuunnitteluun

Erasmus Charter for Higher Education Hakukierros kevät 2013 Anne Siltala, CIMO

Erasmus Charter for Higher Education 2014-2020 Hakukierros kevät 2013 Anne Siltala, CIMO 2/2009 Mikä on Erasmus-peruskirja? Erasmus-peruskirja (Erasmus Charter for Higher Education, ECHE) säilyy korkeakoulun

Erasmus Charter for Higher Education 2014-2020 Hakukierros kevät 2013 Anne Siltala, CIMO 2/2009 Mikä on Erasmus-peruskirja? Erasmus-peruskirja (Erasmus Charter for Higher Education, ECHE) säilyy korkeakoulun

ECVETin soveltuvuus suomalaisiin tutkinnon perusteisiin. Case:Yrittäjyyskurssi matkailualan opiskelijoille englantilaisen opettajan toteuttamana

ECVETin soveltuvuus suomalaisiin tutkinnon perusteisiin Case:Yrittäjyyskurssi matkailualan opiskelijoille englantilaisen opettajan toteuttamana Taustaa KAO mukana FINECVET-hankeessa, jossa pilotoimme ECVETiä

ECVETin soveltuvuus suomalaisiin tutkinnon perusteisiin Case:Yrittäjyyskurssi matkailualan opiskelijoille englantilaisen opettajan toteuttamana Taustaa KAO mukana FINECVET-hankeessa, jossa pilotoimme ECVETiä

C++11 seminaari, kevät Johannes Koskinen

C++11 seminaari, kevät 2012 Johannes Koskinen Sisältö Mikä onkaan ongelma? Standardidraftin luku 29: Atomiset tyypit Muistimalli Rinnakkaisuus On multicore systems, when a thread writes a value to memory,

C++11 seminaari, kevät 2012 Johannes Koskinen Sisältö Mikä onkaan ongelma? Standardidraftin luku 29: Atomiset tyypit Muistimalli Rinnakkaisuus On multicore systems, when a thread writes a value to memory,

Hankkeiden vaikuttavuus: Työkaluja hankesuunnittelun tueksi

Ideasta projektiksi - kumppanuushankkeen suunnittelun lähtökohdat Hankkeiden vaikuttavuus: Työkaluja hankesuunnittelun tueksi Erasmus+ -ohjelman hakuneuvonta ammatillisen koulutuksen kumppanuushanketta

Ideasta projektiksi - kumppanuushankkeen suunnittelun lähtökohdat Hankkeiden vaikuttavuus: Työkaluja hankesuunnittelun tueksi Erasmus+ -ohjelman hakuneuvonta ammatillisen koulutuksen kumppanuushanketta

IAAn InsAcc kokous vakuutussopimusstandardin vaiheesta II ja Standard Subcommitteen kokous Vienissä

Kysymykset pentti.soininen@mandatumlife.fi INSURANCE ACCOUNTING SUBCOMMITTEE Läsnä myös Alessandro D Eri (IASB) Ao. järjestys ei ole käsittely- eikä kysymysjärjestys, vaan periytyy aiemmasta dokusta. 1.

Kysymykset pentti.soininen@mandatumlife.fi INSURANCE ACCOUNTING SUBCOMMITTEE Läsnä myös Alessandro D Eri (IASB) Ao. järjestys ei ole käsittely- eikä kysymysjärjestys, vaan periytyy aiemmasta dokusta. 1.

HARJOITUS- PAKETTI A

Logistiikka A35A00310 Tuotantotalouden perusteet HARJOITUS- PAKETTI A (6 pistettä) TUTA 19 Luento 3.Ennustaminen County General 1 piste The number of heart surgeries performed at County General Hospital

Logistiikka A35A00310 Tuotantotalouden perusteet HARJOITUS- PAKETTI A (6 pistettä) TUTA 19 Luento 3.Ennustaminen County General 1 piste The number of heart surgeries performed at County General Hospital

7.4 Variability management

7.4 Variability management time... space software product-line should support variability in space (different products) support variability in time (maintenance, evolution) 1 Product variation Product

7.4 Variability management time... space software product-line should support variability in space (different products) support variability in time (maintenance, evolution) 1 Product variation Product

2017/S Contract notice. Supplies

Supplies 153936 2017 25/04/2017 S80 - - Supplies - Contract notice - Open procedure I. II. III. IV. VI. -: Medical equipments, pharmaceuticals and personal care products 2017/S 080-153936 Contract notice

Supplies 153936 2017 25/04/2017 S80 - - Supplies - Contract notice - Open procedure I. II. III. IV. VI. -: Medical equipments, pharmaceuticals and personal care products 2017/S 080-153936 Contract notice

Constructive Alignment in Specialisation Studies in Industrial Pharmacy in Finland

Constructive Alignment in Specialisation Studies in Industrial Pharmacy in Finland Anne Mari Juppo, Nina Katajavuori University of Helsinki Faculty of Pharmacy 23.7.2012 1 Background Pedagogic research

Constructive Alignment in Specialisation Studies in Industrial Pharmacy in Finland Anne Mari Juppo, Nina Katajavuori University of Helsinki Faculty of Pharmacy 23.7.2012 1 Background Pedagogic research

Nordea Bank Abp. Nordea Bank Abp

Notice Nordea Bank Abp ISSUANCE by Nordea Bank Abp of instruments listed in Annex 1 Issued pursuant to the Structured Note Programme (the Notes ) Credit Event Notice On 15/10/2018 ISDA s (International

Notice Nordea Bank Abp ISSUANCE by Nordea Bank Abp of instruments listed in Annex 1 Issued pursuant to the Structured Note Programme (the Notes ) Credit Event Notice On 15/10/2018 ISDA s (International

T Statistical Natural Language Processing Answers 6 Collocations Version 1.0

T-61.5020 Statistical Natural Language Processing Answers 6 Collocations Version 1.0 1. Let s start by calculating the results for pair valkoinen, talo manually: Frequency: Bigrams valkoinen, talo occurred

T-61.5020 Statistical Natural Language Processing Answers 6 Collocations Version 1.0 1. Let s start by calculating the results for pair valkoinen, talo manually: Frequency: Bigrams valkoinen, talo occurred

Kysymys 5 Compared to the workload, the number of credits awarded was (1 credits equals 27 working hours): (4)

: (4)") Tilasto T1106120-s2012palaute Kyselyn T1106120+T1106120-s2012palaute yhteenveto: vastauksia (4) Kysymys 1 Degree programme: (4) TIK: TIK 1 25% ************** INF: INF 0 0% EST: EST 0 0% TLT: TLT 0 0% BIO:

Tilasto T1106120-s2012palaute Kyselyn T1106120+T1106120-s2012palaute yhteenveto: vastauksia (4) Kysymys 1 Degree programme: (4) TIK: TIK 1 25% ************** INF: INF 0 0% EST: EST 0 0% TLT: TLT 0 0% BIO:

7. Product-line architectures

7. Product-line architectures 7.1 Introduction 7.2 Product-line basics 7.3 Layered style for product-lines 7.4 Variability management 7.5 Benefits and problems with product-lines 1 Short history of software

7. Product-line architectures 7.1 Introduction 7.2 Product-line basics 7.3 Layered style for product-lines 7.4 Variability management 7.5 Benefits and problems with product-lines 1 Short history of software

VUOSI 2015 / YEAR 2015

VUOSI 2015 / YEAR 2015 Kansainvälisen opetuksen ja tutkimustoiminnan kehittäminen Developing international teaching and research activities Rehtorin strateginen rahoitus vuosille 2014-2016 / Strategic

VUOSI 2015 / YEAR 2015 Kansainvälisen opetuksen ja tutkimustoiminnan kehittäminen Developing international teaching and research activities Rehtorin strateginen rahoitus vuosille 2014-2016 / Strategic

Skene. Games Refueled. Muokkaa perustyyl. napsautt. @Games for Health, Kuopio. 2013 kari.korhonen@tekes.fi. www.tekes.fi/skene

Skene Muokkaa perustyyl. Games Refueled napsautt. @Games for Health, Kuopio Muokkaa alaotsikon perustyyliä napsautt. 2013 kari.korhonen@tekes.fi www.tekes.fi/skene 10.9.201 3 Muokkaa Skene boosts perustyyl.

Skene Muokkaa perustyyl. Games Refueled napsautt. @Games for Health, Kuopio Muokkaa alaotsikon perustyyliä napsautt. 2013 kari.korhonen@tekes.fi www.tekes.fi/skene 10.9.201 3 Muokkaa Skene boosts perustyyl.

RANTALA SARI: Sairaanhoitajan eettisten ohjeiden tunnettavuus ja niiden käyttö hoitotyön tukena sisätautien vuodeosastolla

TURUN YLIOPISTO Hoitotieteen laitos RANTALA SARI: Sairaanhoitajan eettisten ohjeiden tunnettavuus ja niiden käyttö hoitotyön tukena sisätautien vuodeosastolla Pro gradu -tutkielma, 34 sivua, 10 liitesivua

TURUN YLIOPISTO Hoitotieteen laitos RANTALA SARI: Sairaanhoitajan eettisten ohjeiden tunnettavuus ja niiden käyttö hoitotyön tukena sisätautien vuodeosastolla Pro gradu -tutkielma, 34 sivua, 10 liitesivua

Nordea Bank Abp. Nordea Bank Abp

Notice Nordea Bank Abp ISSUANCE by Nordea Bank Abp of instruments listed in Annex 1 Issued pursuant to the Structured Note Programme (the Notes ) Credit Event Notice On 17/12/2018 ISDA s (International

Notice Nordea Bank Abp ISSUANCE by Nordea Bank Abp of instruments listed in Annex 1 Issued pursuant to the Structured Note Programme (the Notes ) Credit Event Notice On 17/12/2018 ISDA s (International

NAO- ja ENO-osaamisohjelmien loppuunsaattaminen ajatuksia ja visioita

NAO- ja ENO-osaamisohjelmien loppuunsaattaminen ajatuksia ja visioita NAO-ENO työseminaari VI Tampere 3.-4.6.2015 Projektisuunnittelija Erno Hyvönen erno.hyvonen@minedu.fi Aikuiskoulutuksen paradigman

NAO- ja ENO-osaamisohjelmien loppuunsaattaminen ajatuksia ja visioita NAO-ENO työseminaari VI Tampere 3.-4.6.2015 Projektisuunnittelija Erno Hyvönen erno.hyvonen@minedu.fi Aikuiskoulutuksen paradigman

Siirtymä maisteriohjelmiin tekniikan korkeakoulujen välillä Transfer to MSc programmes between engineering schools

Siirtymä maisteriohjelmiin tekniikan korkeakoulujen välillä Transfer to MSc programmes between engineering schools Akateemisten asioiden komitea Academic Affairs Committee 11 October 2016 Eija Zitting

Siirtymä maisteriohjelmiin tekniikan korkeakoulujen välillä Transfer to MSc programmes between engineering schools Akateemisten asioiden komitea Academic Affairs Committee 11 October 2016 Eija Zitting

. LIFE+ HAKEMUKSEN VA V L A M L I M ST S E T L E U L 1

. LIFE+ HAKEMUKSEN VALMISTELU 1 HAKULOMAKKEET Hakulomakkeet on jaettu kolmeen osaan: Hallinnolliset A-lomakkeet Tekniset B- ja C-lomakkeet Taloudelliset (F) lomakkeet HALLINNOLLISET (A) LOMAKKEET 2011

. LIFE+ HAKEMUKSEN VALMISTELU 1 HAKULOMAKKEET Hakulomakkeet on jaettu kolmeen osaan: Hallinnolliset A-lomakkeet Tekniset B- ja C-lomakkeet Taloudelliset (F) lomakkeet HALLINNOLLISET (A) LOMAKKEET 2011

Administrative Guidelines for Asia Programme

Administrative Guidelines for Asia Programme Administrative guidelines Guidelines by call / year of receiving funding http://www.cimo.fi/ohjelmat/aasia_ohjelma/osallistujalle Funding can not be used to

Administrative Guidelines for Asia Programme Administrative guidelines Guidelines by call / year of receiving funding http://www.cimo.fi/ohjelmat/aasia_ohjelma/osallistujalle Funding can not be used to

Equality of treatment Public Services

Equality of treatment Public Services Providing high-quality Public Services in Europe based on the values of Protocol 26 (TFEU), Warsaw 12.10.2012 Kristian Siikavirta, Doctor of Law 18.10.2012 1 University

Equality of treatment Public Services Providing high-quality Public Services in Europe based on the values of Protocol 26 (TFEU), Warsaw 12.10.2012 Kristian Siikavirta, Doctor of Law 18.10.2012 1 University

Horisontti 2020 ajankohtaisinfo

Horisontti 2020 ajankohtaisinfo Hanna Vuorinen Kustannusasioiden NCP 1.12.2016 Aiheet Uusi malliavustussopimus ja kommentoitu avustussopimus Malliavustussopimuksen muutokset Art. 4.2. Budjettisiirrot Art.

Horisontti 2020 ajankohtaisinfo Hanna Vuorinen Kustannusasioiden NCP 1.12.2016 Aiheet Uusi malliavustussopimus ja kommentoitu avustussopimus Malliavustussopimuksen muutokset Art. 4.2. Budjettisiirrot Art.

Solvenssi II:n ja IFRS:n Markkinaehtoinen vastuuvelka

Solvenssi II:n ja IFRS:n Markkinaehtoinen vastuuvelka Aktuaariyhdistys, Helsinki Pentti Soininen Lyhenteitä toimijoista Koska esitys sisältää runsaasti viittauksia eri toimijoihin, luetellaan niistä keskeisimpiä:

Solvenssi II:n ja IFRS:n Markkinaehtoinen vastuuvelka Aktuaariyhdistys, Helsinki Pentti Soininen Lyhenteitä toimijoista Koska esitys sisältää runsaasti viittauksia eri toimijoihin, luetellaan niistä keskeisimpiä:

anna minun kertoa let me tell you

anna minun kertoa let me tell you anna minun kertoa I OSA 1. Anna minun kertoa sinulle mitä oli. Tiedän että osaan. Kykenen siihen. Teen nyt niin. Minulla on oikeus. Sanani voivat olla puutteellisia mutta

anna minun kertoa let me tell you anna minun kertoa I OSA 1. Anna minun kertoa sinulle mitä oli. Tiedän että osaan. Kykenen siihen. Teen nyt niin. Minulla on oikeus. Sanani voivat olla puutteellisia mutta

Naisnäkökulma sijoittamiseen. 24.3.2007 Vesa Puttonen

Naisnäkökulma sijoittamiseen 24.3.2007 Vesa Puttonen Miten sukupuolella voi olla mitään tekemistä sijoittamisen kanssa??? Naiset elävät (keskimäärin) pidempään kuin miehet Naiset saavat (keskimäärin) vähemmän

Naisnäkökulma sijoittamiseen 24.3.2007 Vesa Puttonen Miten sukupuolella voi olla mitään tekemistä sijoittamisen kanssa??? Naiset elävät (keskimäärin) pidempään kuin miehet Naiset saavat (keskimäärin) vähemmän

SSTY:n EMC-seminaari. EMC ja sähköisten lääkintälaitteiden standardit. Ari Honkala SESKO ry

SSTY:n EMC-seminaari EMC ja sähköisten lääkintälaitteiden standardit SESKO ry 2016-10-04 Tässä esityksessä käsitellään Yleistä täydentävistä (collateral, -1 sarja, horisontaaliset) ja eritysvaatimuksia

SSTY:n EMC-seminaari EMC ja sähköisten lääkintälaitteiden standardit SESKO ry 2016-10-04 Tässä esityksessä käsitellään Yleistä täydentävistä (collateral, -1 sarja, horisontaaliset) ja eritysvaatimuksia

S Sähkön jakelu ja markkinat S Electricity Distribution and Markets

S-18.3153 Sähkön jakelu ja markkinat S-18.3154 Electricity Distribution and Markets Voltage Sag 1) Kolmivaiheinen vastukseton oikosulku tapahtuu 20 kv lähdöllä etäisyydellä 1 km, 3 km, 5 km, 8 km, 10 km

S-18.3153 Sähkön jakelu ja markkinat S-18.3154 Electricity Distribution and Markets Voltage Sag 1) Kolmivaiheinen vastukseton oikosulku tapahtuu 20 kv lähdöllä etäisyydellä 1 km, 3 km, 5 km, 8 km, 10 km

Pörssiyhtiön tiedottamisen ja sijoittajaviestinnän hyviä käytäntöjä ja haasteita Sisäpiirintieto ja tiedottamisvelvollisuus, Krogerus 27.8.

Pörssiyhtiön tiedottamisen ja sijoittajaviestinnän hyviä käytäntöjä ja haasteita Sisäpiirintieto ja tiedottamisvelvollisuus, Krogerus 27.8.2013 Karla Lindahl, sijoittajasuhdejohtaja, KONE Oyj Kaiken tiedottamisen

Pörssiyhtiön tiedottamisen ja sijoittajaviestinnän hyviä käytäntöjä ja haasteita Sisäpiirintieto ja tiedottamisvelvollisuus, Krogerus 27.8.2013 Karla Lindahl, sijoittajasuhdejohtaja, KONE Oyj Kaiken tiedottamisen

Choose Finland-Helsinki Valitse Finland-Helsinki

Write down the Temporary Application ID. If you do not manage to complete the form you can continue where you stopped with this ID no. Muista Temporary Application ID. Jos et onnistu täyttää lomake loppuun

Write down the Temporary Application ID. If you do not manage to complete the form you can continue where you stopped with this ID no. Muista Temporary Application ID. Jos et onnistu täyttää lomake loppuun

KANNATTAVUUDEN ARVIOINTI JA KEHITTÄMINEN ELEMENTTILIIKETOIMINNASSA

LAPPEENRANNAN TEKNILLINEN YLIOPISTO TEKNISTALOUDELLINEN TIEDEKUNTA Tuotantotalouden koulutusohjelma KANNATTAVUUDEN ARVIOINTI JA KEHITTÄMINEN ELEMENTTILIIKETOIMINNASSA Diplomityöaihe on hyväksytty Tuotantotalouden

LAPPEENRANNAN TEKNILLINEN YLIOPISTO TEKNISTALOUDELLINEN TIEDEKUNTA Tuotantotalouden koulutusohjelma KANNATTAVUUDEN ARVIOINTI JA KEHITTÄMINEN ELEMENTTILIIKETOIMINNASSA Diplomityöaihe on hyväksytty Tuotantotalouden

Ajankohtaista BEPS:stä. Sami Laaksonen Siirtohinnoitteluhankkeen asiakasinfotilaisuus

Ajankohtaista BEPS:stä Sami Laaksonen Siirtohinnoitteluhankkeen asiakasinfotilaisuus 24.10.2014 BEPS G20-valtiot antoivat OECD:lle viime vuonna toimeksiannon kehittää kansainväliseen verotukseen säännöt,

Ajankohtaista BEPS:stä Sami Laaksonen Siirtohinnoitteluhankkeen asiakasinfotilaisuus 24.10.2014 BEPS G20-valtiot antoivat OECD:lle viime vuonna toimeksiannon kehittää kansainväliseen verotukseen säännöt,

Uusi Ajatus Löytyy Luonnosta 4 (käsikirja) (Finnish Edition)

(Finnish Edition)") Uusi Ajatus Löytyy Luonnosta 4 (käsikirja) (Finnish Edition) Esko Jalkanen Click here if your download doesn"t start automatically Uusi Ajatus Löytyy Luonnosta 4 (käsikirja) (Finnish Edition) Esko Jalkanen

Uusi Ajatus Löytyy Luonnosta 4 (käsikirja) (Finnish Edition) Esko Jalkanen Click here if your download doesn"t start automatically Uusi Ajatus Löytyy Luonnosta 4 (käsikirja) (Finnish Edition) Esko Jalkanen

Supplies

Supplies - 239150-2018 05/06/2018 S105 - - Supplies - Contract notice - Open procedure I. II. III. IV. VI. Finland-Oulu: Medical equipments 2018/S 105-239150 Contract notice Supplies Directive 2014/24/EU

Supplies - 239150-2018 05/06/2018 S105 - - Supplies - Contract notice - Open procedure I. II. III. IV. VI. Finland-Oulu: Medical equipments 2018/S 105-239150 Contract notice Supplies Directive 2014/24/EU

Guidebook for Multicultural TUT Users

1 Guidebook for Multicultural TUT Users WORKPLACE PIRKANMAA-hankkeen KESKUSTELUTILAISUUS 16.12.2010 Hyvää käytäntöä kehittämässä - vuorovaikutusopas kansainvälisille opiskelijoille TTY Teknis-taloudellinen

1 Guidebook for Multicultural TUT Users WORKPLACE PIRKANMAA-hankkeen KESKUSTELUTILAISUUS 16.12.2010 Hyvää käytäntöä kehittämässä - vuorovaikutusopas kansainvälisille opiskelijoille TTY Teknis-taloudellinen

Datahub-projekti. Prosessityöryhmä

Datahub-projekti Prosessityöryhmä 8.10.2018 Agenda 8.10.2018 9.00 Kokouksen avaus 9.05 Edellisen kokouksen muistio 9.15 Kotitehtävien läpikäynti (muut kuin risteävät prosessit) 9:30 Risteävien prosessien

Datahub-projekti Prosessityöryhmä 8.10.2018 Agenda 8.10.2018 9.00 Kokouksen avaus 9.05 Edellisen kokouksen muistio 9.15 Kotitehtävien läpikäynti (muut kuin risteävät prosessit) 9:30 Risteävien prosessien

Fighting diffuse nutrient load: Multifunctional water management concept in natural reed beds

PhD Anne Hemmi 14.2.2013 RRR 2013 Conference in Greifswald, Germany Fighting diffuse nutrient load: Multifunctional water management concept in natural reed beds Eutrophication in surface waters High nutrient

PhD Anne Hemmi 14.2.2013 RRR 2013 Conference in Greifswald, Germany Fighting diffuse nutrient load: Multifunctional water management concept in natural reed beds Eutrophication in surface waters High nutrient

National Building Code of Finland, Part D1, Building Water Supply and Sewerage Systems, Regulations and guidelines 2007

National Building Code of Finland, Part D1, Building Water Supply and Sewerage Systems, Regulations and guidelines 2007 Chapter 2.4 Jukka Räisä 1 WATER PIPES PLACEMENT 2.4.1 Regulation Water pipe and its

National Building Code of Finland, Part D1, Building Water Supply and Sewerage Systems, Regulations and guidelines 2007 Chapter 2.4 Jukka Räisä 1 WATER PIPES PLACEMENT 2.4.1 Regulation Water pipe and its

SUOMEN AKTUAARIYHDISTYS Katsaus kansainvälisistä työryhmistä IAA Insurance Accounting Committee

SUOMEN AKTUAARIYHDISTYS Katsaus kansainvälisistä työryhmistä IAA Insurance Accounting Committee Aktuaariyhdistys, Helsinki 11.12.2013, SHV, OP-Pohjola, OP-Palvelut IFRS- ja solvenssiasiantuntija FK:n IFRS-jaoston

SUOMEN AKTUAARIYHDISTYS Katsaus kansainvälisistä työryhmistä IAA Insurance Accounting Committee Aktuaariyhdistys, Helsinki 11.12.2013, SHV, OP-Pohjola, OP-Palvelut IFRS- ja solvenssiasiantuntija FK:n IFRS-jaoston

Smart specialisation for regions and international collaboration Smart Pilots Seminar

Smart specialisation for regions and international collaboration Smart Pilots Seminar 23.5.2017 Krista Taipale Head of Internaltional Affairs Helsinki-Uusimaa Regional Council Internationalisation

Smart specialisation for regions and international collaboration Smart Pilots Seminar 23.5.2017 Krista Taipale Head of Internaltional Affairs Helsinki-Uusimaa Regional Council Internationalisation

Biotie Therapies Corp.

Biotie Therapies Corp. Timo Veromaa, President and CEO EGM 28.11.2006 Future outlook 2006 (1/2) (As presented in the AGM 30 March 2006) Commercialize the European and Asian rights of nalmefene Bring the

Biotie Therapies Corp. Timo Veromaa, President and CEO EGM 28.11.2006 Future outlook 2006 (1/2) (As presented in the AGM 30 March 2006) Commercialize the European and Asian rights of nalmefene Bring the

Esko Kivisaari 14.12.2004

International Actuarial Standards of Practice (IASP) for actuaries dealing with either insurance contracts or investment contracts issued by insurers in connection with IFRSs Esko Kivisaari 14.12.2004

International Actuarial Standards of Practice (IASP) for actuaries dealing with either insurance contracts or investment contracts issued by insurers in connection with IFRSs Esko Kivisaari 14.12.2004

FIS IMATRAN KYLPYLÄHIIHDOT Team captains meeting

FIS IMATRAN KYLPYLÄHIIHDOT 8.-9.12.2018 Team captains meeting 8.12.2018 Agenda 1 Opening of the meeting 2 Presence 3 Organizer s personell 4 Jury 5 Weather forecast 6 Composition of competitors startlists

FIS IMATRAN KYLPYLÄHIIHDOT 8.-9.12.2018 Team captains meeting 8.12.2018 Agenda 1 Opening of the meeting 2 Presence 3 Organizer s personell 4 Jury 5 Weather forecast 6 Composition of competitors startlists

Introduction to Mathematical Economics, ORMS1030

Uiversity of Vaasa, sprig 04 Itroductio to Mathematical Ecoomics, ORMS030 Exercise 6, week 0 Mar 3 7, 04 R ma 0 D5 R5 ti 4 6 C09 R ma 4 6 D5 R6 to 4 C09 R3 ti 08 0 D5 R7 pe 08 0 D5 R4 ti 4 C09 R8 pe 0

Uiversity of Vaasa, sprig 04 Itroductio to Mathematical Ecoomics, ORMS030 Exercise 6, week 0 Mar 3 7, 04 R ma 0 D5 R5 ti 4 6 C09 R ma 4 6 D5 R6 to 4 C09 R3 ti 08 0 D5 R7 pe 08 0 D5 R4 ti 4 C09 R8 pe 0

Information on Finnish Language Courses Spring Semester 2018 Päivi Paukku & Jenni Laine Centre for Language and Communication Studies

Information on Finnish Language Courses Spring Semester 2018 Päivi Paukku & Jenni Laine 4.1.2018 Centre for Language and Communication Studies Puhutko suomea? -Hei! -Hei hei! -Moi! -Moi moi! -Terve! -Terve

Information on Finnish Language Courses Spring Semester 2018 Päivi Paukku & Jenni Laine 4.1.2018 Centre for Language and Communication Studies Puhutko suomea? -Hei! -Hei hei! -Moi! -Moi moi! -Terve! -Terve

PÖRSSISÄÄTIÖN ANALYYTIKKOPANEELI Keskiviikko 11.11. klo 10.00-11.20

PÖRSSISÄÄTIÖN ANALYYTIKKOPANEELI Keskiviikko 11.11. klo 1.-11.2 Jari Harjunpää E. Öhman J:or Securities Finland Ltd +358-9-8866621 jari.harjunpaa@ohmangroup.fi 1 Teemat 21 Maltillista nousua, riski pitkittyvästä

PÖRSSISÄÄTIÖN ANALYYTIKKOPANEELI Keskiviikko 11.11. klo 1.-11.2 Jari Harjunpää E. Öhman J:or Securities Finland Ltd +358-9-8866621 jari.harjunpaa@ohmangroup.fi 1 Teemat 21 Maltillista nousua, riski pitkittyvästä

TIEKE Verkottaja Service Tools for electronic data interchange utilizers. Heikki Laaksamo

TIEKE Verkottaja Service Tools for electronic data interchange utilizers Heikki Laaksamo TIEKE Finnish Information Society Development Centre (TIEKE Tietoyhteiskunnan kehittämiskeskus ry) TIEKE is a neutral,

TIEKE Verkottaja Service Tools for electronic data interchange utilizers Heikki Laaksamo TIEKE Finnish Information Society Development Centre (TIEKE Tietoyhteiskunnan kehittämiskeskus ry) TIEKE is a neutral,

Travel Getting Around

- Location Olen eksyksissä. Not knowing where you are Voisitko näyttää kartalta missä sen on? Asking for a specific location on a map Mistä täällä on? Asking for a specific...wc?...pankki / rahanvaihtopiste?...hotelli?...huoltoasema?...sairaala?...apteekki?...tavaratalo?...ruokakauppa?...bussipysäkki?

- Location Olen eksyksissä. Not knowing where you are Voisitko näyttää kartalta missä sen on? Asking for a specific location on a map Mistä täällä on? Asking for a specific...wc?...pankki / rahanvaihtopiste?...hotelli?...huoltoasema?...sairaala?...apteekki?...tavaratalo?...ruokakauppa?...bussipysäkki?

SIJOITUSRISKIEN TARKASTELU 1/2 1

Disclaimer This material has been prepared by Sunduka Oy, a Finnish limited liability company (the Company ), solely for the purpose of providing prospective investors with general financial and other

Disclaimer This material has been prepared by Sunduka Oy, a Finnish limited liability company (the Company ), solely for the purpose of providing prospective investors with general financial and other

Data protection template

Data protection template Aihe: rekisteriseloste ja informointipohja Topic: information about the register and information to users (related to General Data Protection Regulation (GDPR) (EU) 2016/679) Mallina

Data protection template Aihe: rekisteriseloste ja informointipohja Topic: information about the register and information to users (related to General Data Protection Regulation (GDPR) (EU) 2016/679) Mallina

Horizon 2020 SME Instrument

Horizon 2020 SME Instrument Miksi hakea rahoitusta SME Instrumentista Rahoitusinstrumentti tarjoaa tukea 70% yrityksen tuotekehitykseen tai liiketoimintasuunnitelman rakentamiseen Pk- yrityksille ja Startupeille,

Horizon 2020 SME Instrument Miksi hakea rahoitusta SME Instrumentista Rahoitusinstrumentti tarjoaa tukea 70% yrityksen tuotekehitykseen tai liiketoimintasuunnitelman rakentamiseen Pk- yrityksille ja Startupeille,

Riskienhallintajärjestelmä, Riskienhallintatoiminto ja Aktuaaritoiminto

Riskienhallintajärjestelmä, Riskienhallintatoiminto ja Aktuaaritoiminto Aktuaariyhdistyksen solvenssiseminaari 18.5.2010 Janne Sorainen 18.5.2010 18.5.2010 1 System of Governance (Hallintojärjestelmä)

Riskienhallintajärjestelmä, Riskienhallintatoiminto ja Aktuaaritoiminto Aktuaariyhdistyksen solvenssiseminaari 18.5.2010 Janne Sorainen 18.5.2010 18.5.2010 1 System of Governance (Hallintojärjestelmä)

Increase of opioid use in Finland when is there enough key indicator data to state a trend?

Increase of opioid use in Finland when is there enough key indicator data to state a trend? Martta Forsell, Finnish Focal Point 28.9.2015 Esityksen nimi / Tekijä 1 Martta Forsell Master of Social Sciences

Increase of opioid use in Finland when is there enough key indicator data to state a trend? Martta Forsell, Finnish Focal Point 28.9.2015 Esityksen nimi / Tekijä 1 Martta Forsell Master of Social Sciences

Rekisteröiminen - FAQ

Rekisteröiminen - FAQ Miten Akun/laturin rekisteröiminen tehdään Akun/laturin rekisteröiminen tapahtuu samalla tavalla kuin nykyinen takuurekisteröityminen koneille. Nykyistä tietokantaa on muokattu niin,

Rekisteröiminen - FAQ Miten Akun/laturin rekisteröiminen tehdään Akun/laturin rekisteröiminen tapahtuu samalla tavalla kuin nykyinen takuurekisteröityminen koneille. Nykyistä tietokantaa on muokattu niin,

Wärtsilä Corporation. Interim Report January-June 2003 Ole Johansson President & CEO. 31 July Wärtsilä

Wärtsilä Corporation Interim Report January-June 2003 Ole Johansson President & CEO 31 July 2003 Group structure Power Divisions Engine division Marine Power Plants Service Holding Assa Abloy 7.6% 2 Group

Wärtsilä Corporation Interim Report January-June 2003 Ole Johansson President & CEO 31 July 2003 Group structure Power Divisions Engine division Marine Power Plants Service Holding Assa Abloy 7.6% 2 Group

Co-Design Yhteissuunnittelu

Co-Design Yhteissuunnittelu Tuuli Mattelmäki DA, associate professor Aalto University School of Arts, Design and Architecture School of Arts, Design and Architecture design with and for people Codesign

Co-Design Yhteissuunnittelu Tuuli Mattelmäki DA, associate professor Aalto University School of Arts, Design and Architecture School of Arts, Design and Architecture design with and for people Codesign

Vuosi 2006. Jukka Rinnevaara Toimitusjohtaja

Vuosi 2006 Jukka Rinnevaara Toimitusjohtaja 1 Disclaimer This presentation is confidential and is intended solely for the use of the recipients of the presentation in connection with their consideration

Vuosi 2006 Jukka Rinnevaara Toimitusjohtaja 1 Disclaimer This presentation is confidential and is intended solely for the use of the recipients of the presentation in connection with their consideration