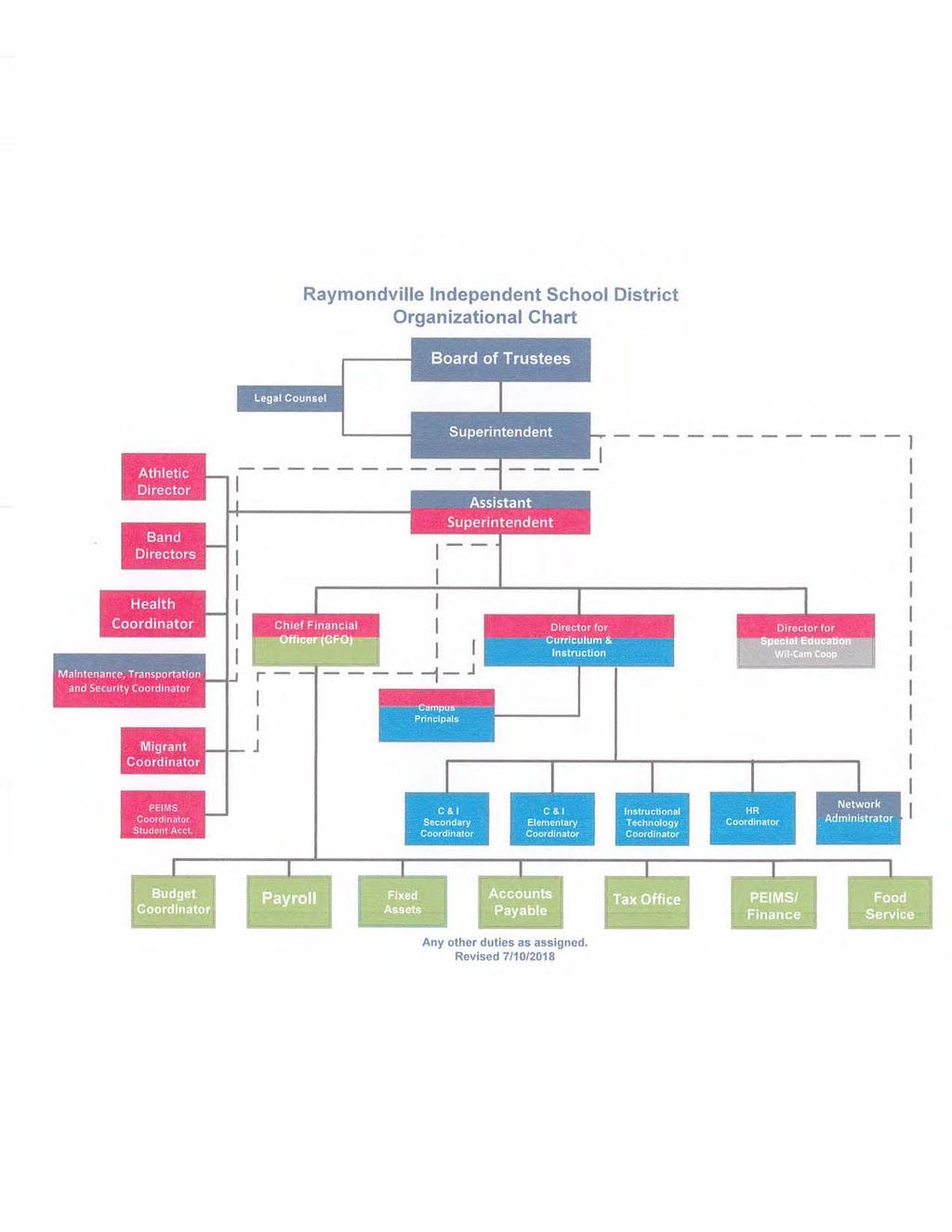

Raymondville ISD. It All Starts Here!

|

|

|

- Tuula Kivelä

- 6 vuotta sitten

- Katselukertoja:

Transkriptio

1 Raymondville ISD It All Starts Here!

2 Prepared by: Business Office

3 Exhibit COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED JUNE 30, 2018 TABLE OF CONTENTS Certificate of Board 1 Independent Auditors Report 2 FINANCIAL SECTION Management s Discussion and Analysis 5 Basic Financial Statements Government-wide Statements: A-1 Statement of Net Position 12 B-1 Statement of Activities 13 Governmental Fund Financial Statements: C-1 Balance Sheet 14 C-2 Reconciliation of the Governmental Funds Balance Sheet to the 16 Statement of Net Position 15 C-3 Statement of Revenues, Expenditures, and Changes in Fund Balances 17 C-4 Reconciliation of the Governmental Funds Statement of Revenues, 19 Expenditures, and Changes in Fund Balances to the Statement of Activities Fiduciary Fund Financial Statements: E-1 Statement of Fiduciary Net Position 20 Notes to the Financial Statements 21 Required Supplementary Information G-1 Schedule of Revenues, Expenditures, and Changes in Fund Balance Budget and Actual General Fund 52 G-2 Schedule of the District s Proportionate Share of the Net Pension Liability 53 G-3 Schedule of District Contributions Teacher Retirement System 54 G-4 Schedule of the District s Proportionate Share of the Net OPEB Liability 55 G-5 Schedule of District OPEB Contributions Teacher Retirement System 56 Notes to Required Supplementary Information 57 Combining Statements Nonmajor Governmental Funds: Special Revenue Descriptions 58 H-1 Combining Balance Sheet 59 H-2 Combining Statement of Revenues, Expenditures, and Changes in Fund Balances 62 H-3 Combining Statement of Changes in Assets and Liabilities all Agency Funds 65 Required TEA Schedules J-1 Schedule of Delinquent Taxes Receivable 66 J-4 Schedule of Revenues, Expenditures, and Changes in Fund Balance Budget and Actual National School Breakfast and Lunch Program 68 J-5 Schedule of Revenues, Expenditures, and Changes in Fund Balance Budget and Actual Debt Service Fund 69 Page i

4 Schedule COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED JUNE 30, 2018 TABLE OF CONTENTS CONTINUED STATISTICAL SECTION Page Statistical Section Overview 70 Government-wide Information 1 Net Assets by Component Last Ten Years 71 2 Governmental Activities Expenses and Program Revenues 73 3 General Revenues and Changes in Net Position 75 Fund Information 4 Fund Balances Governmental Funds Last Ten Years 77 5 Governmental Fund Revenues by Source 78 6 Governmental Fund Expenditures by Function 80 7 Governmental Funds Other Sources, Uses and Changes in Fund Balance 82 8 Governmental Fund Expenditures by Function Per Average Daily Attendance 84 Revenue Capacity Information 9 Assessed and Estimated Actual Value of Property Property Tax Levies and Collections Allocation of Property Tax Rates and Levies Property Tax Rates Direct and Overlapping Governments (Per $100 Assessed Valuation)-Last Ten Years Principal Property Taxpayer Current Year and Ten Years Prior 92 Debt Capacity Information 14 Outstanding Debt by Type Last Ten Years Direct and Overlapping Debt General Obligation Bonds Computation of Legal Debt Margin Last Ten Years Ratio of Net General Obligation Bonded Debt to Estimated Actual Value and Per Average Daily Membership Last Ten Years Ratio of Annual Debt Service for General Bonded Debt To Total General Fund Expenditures Last Ten Years 100 Demographic and Economic Information 19 Principal Employers Current Year and Ten Years Ago Construction and Property Values Last Ten Years Economic and Demographic Statistics Last Ten Years 104 Operating Information 22 Work Force Composition by Employee Classification Last Ten Years Schedule of Teacher Information Last Ten Years Schedule of Attendance and Membership Last Ten Years Operating Statistics Last Ten Years Schedule of Student Information Last Ten Years Schedule of School Buildings Last Ten Years 110 ii

5 COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED JUNE 30, 2018 TABLE OF CONTENTS CONTINUED Schedule Page SINGLE AUDIT SECTION Independent Auditors Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards 111 Independent Auditors Report on Compliance for Each Major Federal Program and Report on Internal Control Over Compliance in Accordance with the Uniform Guidance 113 K-1 Schedule of Expenditures of Federal Awards 115 Notes to Schedule of Expenditures of Federal Awards 116 Schedule of Findings and Questioned Costs 117 Summary Schedule of Prior Audit Findings 118 iii

6

7 419 FM 3168, Raymondville, Texas Phone: (956) Business Office November 13, 2018 Mr. Stetson Roane, Superintendent Members of the Board of Trustees Raymondville Independent School District Raymondville, Texas Dear Mr. Roane and Members: Every year public school districts throughout the state are required to present within one-hundred fifty days of the end of each fiscal year an audited set of financial statements. These financial statements are to be presented in conformity with generally accepted accounting principles (GAAP) and audited by a licensed certified public accountant in accordance with generally accepted auditing standards. Pursuant to that requirement, we are pleased to present the Raymondville Independent School District Comprehensive Annual Financial Report (CAFR) for the year ending June 30, This report consists of management s representation concerning the finances of the District. The District s audited financial statements of the governmental activities, each major fund, and the aggregate remaining fund information are presented in conformity with requirements established by the Texas Education Agency in their Financial Accountability Systems Resource Guide. Responsibility for both the accuracy of the presented data and the completeness and fairness of the presentation, including all disclosures contained in the report, rests solely with the District. To provide a reasonable basis for making these representations, management of the District has established a comprehensive internal control framework that is designed both to protect the government s assets from loss, theft, or misuse and to compile sufficient reliable information for the preparation of the District s financial statements in conformity with GAAP. Because the cost of internal controls should not outweigh their benefits, the District s comprehensive framework of internal controls has been designed to provide reasonable rather than absolute assurance that the financial statements will be free from material misstatement. As management, we assert that, to the best of our knowledge and belief, this financial report is complete and reliable in all material respects. The District s financial statements have been audited by Pattillo, Brown & Hill, L.L.P. and their opinion letter is hereby made part of this report. The goal of the independent audit was to provide reasonable assurance that the financial statements of Raymondville Independent School District for iv

8 the fiscal year ended June 30, 2018, are free of material misstatement and are presented in conformity with generally accepted accounting principles (GAAP). The independent audit involves examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements; assessing the accounting principles used and significant estimates made by management; and evaluating the overall financial statement presentation. The independent auditor concluded, based upon the audit, that there was a reasonable basis for rendering an unmodified opinion that the District s financial statements for the fiscal year ended June 30, 2018, are fairly presented in conformity with GAAP. The independent auditors report is presented as the first component of the financial section of this report. The independent audit of the financial statements of the District was part of a broader, federally mandated Single Audit designated to meet the special needs of federal grantor agencies. The standards governing Single Audit engagements require the independent auditor to report not only on the fair presentation of the financial statement, but also on the audited government s internal controls and compliance with legal requirement, with special emphasis on internal controls and legal requirements involving the administration of federal awards. Information related to this single audit, including a schedule of expenditures of federal awards, the independent auditors reports on the internal controls and compliance with applicable laws and regulations, and a schedule of findings and questioned costs are included in the Federal Awards Section of the report. GAAP requires that management provide a narrative introduction, overview, and analysis to accompany the basic financial statements in the form of Management s Discussion and Analysis (MD&A). This letter of transmittal is designed to complement MD&A and should be read in conjunction with it. The District s MD&A can be found immediately following the report of the independent auditors. This comprehensive annual financial report consists of four major sections: (1) the Introductory Section which describes our District and the contents of the report; (2) the Financial Section which contains the basic financial statements and notes, combining schedules and required TEA schedules; (3) the Statistical Section which shows prior years information for comparison purposes and other general information; and (4) the Federal Awards Section, as required. Profile of the Government The District is a political subdivision of the State of Texas governed and operating as an independent school district under the laws thereof. The District primarily services the City of Raymondville which is known as the Gateway to the Rio Grande Valley. The District encompasses approximately 3.8 square miles in Willacy County, Texas. The District is governed by a seven-member Board of Trustees (the Board ) composed of District residents, who are elected by voters of the District. The Board is responsible for managing and governing the schools of the District, including the adoption of goals and objectives for the District, reviewing and acting on policies, adopting an annual budget, levying and collecting District taxes, hiring school personnel as recommended by the superintendent, approving salary schedules, adopting District policies and setting directions for curriculum, and reporting to the public on the District s progress. The District s Superintendent of Schools and staff assist the Board with financial and administrative matters and oversee the day-to-day operations of the District. v

9 Services Provided The District provides a full range of educational services appropriate to grade levels prekindergarten through twelve for its approximate 2,050 students. These include regular and enriched academic education, special education for students with disabilities, occupational education, bilingual instruction for those with limited English proficiency and specialized instruction for disadvantaged students. These basic programs are supplemented by additional offerings in the fine arts and athletics. Budgetary Controls On an annual basis, the District presents the Board of Trustees with the proposed budgets for the General Operating Fund, the Debt Service Fund, and the Food Service Fund for approval as required by the Texas Education Code and as described in the Texas Education Agency s Financial Accountability Systems Resource Guide. The proposed budget is presented to the Board summarized at the function level for each of the funds above. The Board is required to hold a public hearing on the proposed budget and to adopt a final budget no later than June 30 th, the close of the District s fiscal year. After adoption of the budget, the appropriation amounts are entered into the District s accounting and encumbrance system and monitoring of the expenditures and encumbrances in relation to the approved budget begins. Budget managers have the authority to approve budget transfers anytime during the year. A budget transfer is the movement of appropriations between budget line items within the same function. Any request to move appropriations between budget line items to different functions is considered a budget amendment. Any budget amendment requested by budget managers requires Board approval. Expenditure requests will not be processed unless appropriations are available in the line item. The District feels that the budgetary controls currently in place are adequate to ensure that expenditures remain within the approved budget and that the District complies with regulations established by the Texas Education Code and the Financial Accountability Systems Resource Guide. Enrollment Raymondville I.S.D is a Title I District and had a total enrollment of 2,088 students for the school year. Of these students, 98.6% are Hispanic, 1.0% White, 86.02% of the students are economically disadvantaged, 58.4% of the students are At-Risk, and 7.1% of all students are identified as Limited English Proficient language learners. The breakdown of our student membership is as follows: Pre-K 157 K TOTAL 2,088 vi

10 Average daily attendance has been stable and with a small decline in the past few years. ADA is expected to slightly increase for the fiscal year. Factors Affecting Financial Condition The information presented in the financial statements is perhaps best understood when it is considered from the broader perspective of the specific environment within which the District operates. Local Economy Raymondville is the county seat of Willacy County, Texas and is strategically positioned along Interstate 69/US Route 77. Agricultural production, correctional facilities, transportation, energy, and service sector continue to play a major role in the Raymondville area economy. Long-term Financial Planning and Major Initiatives The District continues to maintain a healthy General Fund Balance. The District has maintained the fund balance to ensure that needed resources are available when required to meet unexpected revenue shortfalls and one-time expenditures that may exceed the annual available resources. If certain events occur during the year, the District may react with appropriate budget changes and or amendments as per CE (Local) Policy, The expenditure of funds shall be under the direction of the Superintendent or designee who shall ensure that funds are expended in accordance with the adopted budget. Local funding is expected to increase slightly over the next few years due to an increase in new commercial construction and appraisal values. The District s maintenance and operations tax rate for tax year 2017 is $1.17 per $100 valuation. State funding for the general fund is about 61.4% of the total general fund revenue. District Voters approved a Tax Ratification Election (TRE) on September 9, The total tax rate decreased by $ from $ to $ Estimated additional revenues due to the TRE are approximately $1.7 million per year. Federal funding is expected to decrease due to the sequestration of federal funds at the national level. Grant funding plays an important role as a resource to supplement regular funding and to expand programs needed for greater academic achievement. The District is focusing on greater efficiency through the use of technology to help reduce labor and time-consuming paperwork. Cash Management Policies and Practices The District is required to execute a depository agreement with a banking institution for a period of two years. Competitive bidding is mandated and state law sets general terms. The District s investment policy is to minimize credit and market risks while maintaining a competitive yield on its portfolio. All deposits were secured by the Federal Deposit Insurance Corporation (FDIC) and by vii

11 pledged securities. All investments must be in compliance with the guidelines set by the Public Funds Investments Act. The act set the type of investments governmental entities can make. The District has an active cash management program in prudently investing available cash. Cash temporarily idle during the year was invested in pool investments. The District has investments in the First Public LoneStar investment pool. Pension Plan The District contributes to the Teacher Retirement System of Texas (TRS), a public employee, costsharing multiple employer defined benefit pension plan. Under this plan, all risks and costs are not shared by the District but are a liability of the State of Texas. Additional information on the District s pension arrangements can be found in the Notes to the Financial Statements. Property Tax Rate The District total property tax rate is $1.310 per $100 of property taxable value for fiscal year ending June 30, On September 9, 2017, District Voters approved a Tax Ratification Election that would set the tax rate to $1.310 per $100 of property taxable value. The District has maintained one of the lowest school property tax rates in our area. The District has been able to maintain a low tax rate due to the assistance from the State and Federal government in subsidizing annual debt payment for school bonds. The District s property tax rate will again be $1.310 per $100 of property taxable value for fiscal year ending June 30, School FIRST Rating The Schools FIRST (Financial Accountability Rating System of Texas), was developed by the Texas Education Agency in response to Senate Bill 875 passed in The primary goal of Schools FIRST is to achieve quality performance in the management of school districts' financial resources, a goal made more significant due to the complexity of the State's school finance system. The Raymondville Independent School District received a "Superior" rating under Texas' Schools FIRST financial accountability rating system for the fiscal year. The Superior rating was the State's highest, demonstrating the quality of the school district's financial management and reporting system. The primary goal of School FIRST is to achieve quality performance in the management of school district s financial resources. This goal is now more significant due to the complexity of accounting associated with the Texas school finance system. Debt Service Debt Service is a major area of cost due to the District s building program which is primarily financed by the sale of general obligation bonds. The Texas Education Code (TEC) authorizes the District to issue negotiable coupon bonds to construct, acquire, or equip school buildings, to purchase necessary sites, or to acquire or refinance property financed under a contract entered into under the Public Property Finance Act. The District is further authorized to levy and assess annual ad valorem taxes sufficient to pay the principal and interest on the bonds as they become due. The District s primary objective in debt management is to keep the level of indebtedness within available resources and within legal debt limitations. All bond elections are held in accordance with statutory viii

12 ix

13 x

14 xi

15 1

16

17 INDEPENDENT AUDITORS REPORT The Board of Trustees of Raymondville Independent School District Raymondville, Texas Report on the Financial Statements We have audited the accompanying financial statements of the governmental activities, each major fund, and the aggregate remaining fund information of Raymondville Independent School District, as of and for the year ended June 30, 2018, and the related notes to the financial statements, which collectively comprise Raymondville Independent School District s basic financial statements as listed in the table of contents. Management s Responsibility for the Financial Statements Raymondville Independent School District s management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. 2

18 An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions. Opinions In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, each major fund, and the aggregate remaining fund information of Raymondville Independent School District, as of June 30, 2018, and the respective changes in financial position and, where applicable, cashflows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America. Change in Accounting Principle As discussed in the notes to the financial statements, in fiscal year 2018 the District adopted new accounting guidance, Governmental Accounting Standards Board (GASB) Statement No. 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions. Our opinion is not modified with respect to this matter. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the management s discussion and analysis, budgetary comparison, pension and OPEB information to be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. 3

19 Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise Raymondville Independent School District s basic financial statements. The combining statements, required TEA schedules and the Schedule of Expenditures of Federal Awards, as required by the audit requirements of Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), are presented for purposes of additional analysis and are not a required part of the basic financial statements. The combining statements, required TEA schedules and the Schedule of Expenditures of Federal Awards are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, The combining statements, required TEA schedules and the Schedule of Expenditures of Federal Awards are fairly stated in all material respects in relation to the basic financial statements as a whole. The introductory and statistical sections have not been subjected to the auditing procedures applied in the audit of the financial statements and accordingly, we do not express an opinion or provide any assurance on them. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated November 13, 2018, on our consideration of Raymondville Independent School District s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is solely to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Raymondville Independent School District s internal control over financial reporting and compliance. Brownsville, Texas November 13,

20 MANAGEMENT S DISCUSSION AND ANALYSIS This section of Raymondville I.S.D. s annual financial report presents our discussion and analysis of the District s financial performance during the year ended June 30, Please read it in conjunction with the District s financial statements, which follow this section. FINANCIAL HIGHLIGHTS The District s total combined net position was $6,362,628 at June 30, This is a decrease of $16,663,511 from the prior year. This significant decrease is a direct result of the implementation of GASB 75 that required a prior period adjustment of $20,658,875. See Note O for additional details. During the year, the District s expenses were $892,633 less than the $28,814,940 generated in taxes and other revenues for governmental activities. The general fund reported a fund balance this year of $10,225,270. The District received a Superior Rating for the Financial Integrity Rating System of Texas (FIRST) for This rating rates quality performance in the management of school district s financial resources. OVERVIEW OF THE FINANCIAL STATEMENTS This annual report consists of three parts management s discussion and analysis (this section), the basic financial statements, and required supplementary information. The basic financial statements include two kinds of statements that present different views of the District: Figure A-1, Required Components of the District s Annual Financial Report The first two statements are government-wide financial statements that provide both long-term and short-term information about the District s overall financial status. The remaining statements are fund financial statements that focus on individual parts of the government, reporting the District s operations in more detail than the government-wide statements. The governmental funds statements tell how general government services were financed in the short term as well as what remains for future spending. Proprietary fund statements offer short- and long-term financial information about the activities the government operates like businesses, such as food service. Fiduciary fund statements provide information about the financial relationships in which the District acts solely as a trustee or agent for the benefit of others, to whom the resources in question belong. The financial statements also include notes that explain some of the information in the financial statements and provide more detailed data. The statements are followed by a section of required supplementary information that further explains and supports the information in the financial statements. Figure A-1 shows how the required parts of this annual report are arranged and related to one another. 5

21 Figure A-2 summarizes the major features of the District s financial statements, including the portion of the District government they cover and the types of information they contain. The remainder of this overview section of management s discussion and analysis explains the structure and contents of each of the statements. Government-wide Statements The government-wide statements report information about the District as a whole using accounting methods similar to those used by private-sector companies. The statement of net position includes all of the government s assets and liabilities. All of the current year s revenues and expenses are accounted for in the statement of activities regardless of when cash is received or paid. MANAGEMENT S DISCUSSION AND ANALYSIS - CONTINUED The two government-wide statements report the District s net position and how they have changed. Net position the difference between the District s assets and liabilities is one way to measure the District s financial health or position. In fiscal year 2018, the District adopted the Governmental Accounting Standards Board Statement No. 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions which superseded GASB Statement No. 45. Statement No. 75 establishes financial reporting standards and/or accounting standards for state and local government defined other postemployment benefit (OPEB) plans and defined contribution OPEB plans. Statement No. 75 requires that, at transition, a government recognizes a beginning deferred outflow of resources for its OPEB contributions, if any, made subsequent to the measurement date of the beginning net OPEB liability. The effect of the adoption of this statement has no impact on the District's governmental fund financial statements. However, adoption has resulted in certain changes to the presentation of the District's government-wide financial statements. More information on the adoption of this statement and the District's OPEB plan is available in Note K and Note L. Over time, increases or decreases in the District s net position are an indicator of whether its financial health is improving or deteriorating, respectively. To assess the overall health of the District, one needs to consider additional nonfinancial factors such as changes in the District s tax base The government-wide financial statements of the District include the Governmental activities. Most of the District s basic services are included here, such as instruction, extracurricular activities, curriculum and staff development, health services and general administration. Property taxes and grants finance most of these activities. Fund Financial Statements The fund financial statements provide more detailed information about the District s most significant funds not the District as a whole. Funds are accounting devices that the District uses to keep track of specific sources of funding and spending for particular purposes. Some funds are required by State law and by bond covenants. The Board of Trustees establishes other funds to control and manage money for particular purposes or to show that it is properly using certain taxes and grants. The District has the following kinds of funds: Type of Statements Government-wide Governmental Funds Fund Statements Proprietary Funds Fiduciary Funds Entire Agency s government The activities of the district Activities the district that are not proprietary or operates similar to private fiduciary businesses: self insurance Scope Figure A-2. Major Features of the District's Government-wide and Fund Financial Statements Required financial statements Accounting basis and measurement focus Type of asset/liability information Type of inflow/outflow information (except fiduciary funds) and the Agency's component units Instances in which the district is the trustee or agent for someone else's resources Statement of net assets Balance sheet Statement of net assets Statement of fiduciary net assets Statement of activities Statement of revenues, Statement of revenues, Statement of changes expenditures & changes expenses and changes in in fiduciary net assets in fund balances fund net assets Accrual accounting and economic resources focus All assets and liabilities, both financial and capital, short-term and long-term All revenues and expenses during year, regardless of when cash is received or paid Modified accrual accounting and current financial resources focus Only assets expected to be used up and liabilities that come due during the year or soon thereafter; no capital assets included Revenues for which cash is received during or soon after the end of the year; expenditures when goods or services have been received and payment is due during the year or soon thereafter Statement of cash flows Accrual accounting and economic resources focus All assets and liabilities, both financial and capital, and short-term and longterm All revenues and expenses during year, regardless of when cash is received or paid Accrual accounting and economic resources focus All assets and liabilities, both short-term and longterm; the Agency's funds do not currently contain capital assets, although they can All revenues and expenses during year, regardless of when cash is received or paid Governmental funds Most of the District s basic services are included in governmental funds, which focus on (1) how cash and other financial assets that can readily be converted to cash flow in and out and (2) the balances left at yearend that are available for spending. Consequently, the governmental fund statements provide a detailed short-term view that helps you determine whether there are more or fewer financial resources that can be spent in the near future to finance the District s programs. Because this information does not encompass the additional long- 6

between them. Proprietary funds Services for which the District charges customers a fee are generally reported in proprietary funds.")

22 MANAGEMENT S DISCUSSION AND ANALYSIS - CONTINUED term focus of the government-wide statements, we provide additional information at the bottom of the governmental funds statement, or on the subsequent page, that explain the relationship (or differences) between them. Proprietary funds Services for which the District charges customers a fee are generally reported in proprietary funds. Proprietary funds, like the government-wide statements, provide both long-term and short-term financial information. Fiduciary funds The District is the trustee, or fiduciary, for certain funds. It is also responsible for other assets that because of a trust arrangement can be used only for the trust beneficiaries. The District is responsible for ensuring that the assets reported in these funds are used for their intended purposes. All of the District s fiduciary activities are reported in a separate statement of fiduciary net position and a statement of changes in fiduciary net position. We exclude these activities from the District s government-wide financial statements because the District cannot use these assets to finance its operations. FINANCIAL ANALYSIS OF THE DISTRICT AS A WHOLE The District s combined net position were $5,837,120 as of June 30, (See Table A-1). Table A-1 Raymondville Independent School District s Net Position (in thousands of dollars) Governmental Activities Current & other assets $ 14,184 $ 12,968 Capital assets 34,251 35,615 Total assets 48,435 48,583 Deferred outflows of resources 1,305 1,784 Current liabilities 2,880 1,718 Long-term liabilities 34,209 24,719 Total liabilities 37,089 26,437 Deferred inflows of resources 6, Net position: Net investment in capital assets 17,298 17,669 Restricted 2,049 1,829 Unrestricted (12,984) 3,528 Total net position $ 6,363 $ 23,026 Net position may serve over time as a useful indicator of a government s financial position. The assets and deferred outflows of resources of the District exceeded its liabilities at the close of the most recent fiscal year by $6,362,628. Approximately $17.3 million of Raymondville ISD s net position reflects the investment in capital assets (e.g., land, buildings, machinery, and equipment) less any related debt used to acquire those assets that is still outstanding. Raymondville ISD uses these capital assets to provide services to students; consequently, these assets are not available for future spending. Although the Raymondville ISD s investment in capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. An additional portion of the net position (approximately $2 million) represents resources that are subject to external restrictions on how they may be used. The remaining balance of unrestricted net position ($ million) may be used to meet the government s ongoing obligations to students and creditors. Changes in net position Raymondville ISD s net position decreased by $16,663,511 during the current fiscal year. This significant decrease is a direct result of the implementation of GASB 75 that required a prior period adjustment of $20,658,875. See Note O for additional details. The District s total revenues were $25,095,799. A portion, 12.7% of the District s revenue comes from taxes, 57.8% comes from state aid formula grants, while only 4.9% relates to charges for services as reflected in Figure A-5. Unrestricted net position reflects a deficit created by a prior period adjustment resulting from the implementation of GASB 75 in the current fiscal year for OPEB. Although the District reports a deficit, the deficit is primarily due to reporting the District's proportionate share of the net OPEB liability. The total district liability is reported in the governmental activities; however, the actual liability does not require the use of current resources at the fund level, which results in a timing difference since the TRS-Care plan is funded on a pay-as-you-go basis. The District has made all contractually required 7

23 MANAGEMENT S DISCUSSION AND ANALYSIS - CONTINUED contributions as noted in the required supplementary information and has sufficient fund balance to meet the District's ongoing obligations to students and creditors. Governmental Activities As reflected in Table A-2 and Figure A-4: Property tax rates decreased from to /$100 during the current fiscal year ended June 30, Property taxable values increased by 15.5% from the prior year. The cost of all governmental activities this year was $21,100,435, a decrease of $6,645,828 due to the allocation of GASB 75 liabilities and expenditures. However, the amount that our taxpayers paid for these activities through property taxes was $3,187,617. Some of the cost was paid by those who directly benefited from the programs ($1,236,530) or by grants and contributions ($5,623,715). Grants and contributions decreased from the prior year primarily due to adjustments to revenue for implementation of GASB 75. The decrease in functional expenses is primarily due to adjustments to functional expenses to record the State's negative on-behalf contributions for OPEB in conjunction with the implementation of GASB 75. Table A-2 Changes in Raymondville Independent School District s Net position (in thousands of dollars) Governmental Activities Program Revenues: Charges for Services $ 1,237 $ 951 Operating Grants and Contributions 5,624 6,910 Capital Grants and Contributions General Revenues Property Taxes 3,187 3,086 State Aid Formula 13,247 14,310 Investment Earnings Other 1,663 2,040 Total Revenues 25,096 27,363 Instruction 9,652 13,930 Instructional Resources and Media Services Curriculum Dev. And Instructional Staff Dev Instructional Leadership School Leadership 1,109 1,639 Guidance, Counseling and Evaluation Services 804 1,139 Social Work Services Health Services Student (Pupil) Transportation Food Services 1,803 1,861 Curricular/Extracurricular Activities 1,093 1,294 General Administration 1,019 1,084 Plant Maintenance & Operations 2,765 2,873 Security & Monitoring Services Data Processing Services Community Services Debt Service Contracted Instructional Services Between Schools (284) - Payments Related to Shared Services Arrangements Other Governmental Charges Total Expenses 21,100 27,745 $10,000 $9,000 $8,000 $7,000 $6,000 $5,000 $4,000 $3,000 $2,000 $1,000 $- Figure A-4 Raymondville ISD Expenses FY Instruction $ in thousands Instr Resources Curriculum Dev Inst Leadership School Leadership Counseling Social Work Health Services Transportation Food Services Curricular/Extra Administration Plant Maint Security Data Processing Services Community Services Debt Service Contracted Instructional Services Between Schools Payments Related to Shared Svc. Arrangements Other Governmental Charges Increase (Decrease) in Net position $ 3,996 $ (383) 8

. The net cost reflects what was funded by state revenues as well as local tax dollars.")

24 MANAGEMENT S DISCUSSION AND ANALYSIS - CONTINUED Table A-3 presents the cost of each of the District s largest functions, as well as each function s net cost (total cost less fees generated by the activities and intergovernmental aid). The net cost reflects what was funded by state revenues as well as local tax dollars. Table A-3 Net Cost of Selected District Functions (in thousands of dollars) Total Cost of Services % Change Net Cost of Services % Change Instruction 9,953 13,930 (30.7%) (7,709) 10,485 (166.9%) School administration 1,109 1,640 (32.4%) (1,068) 1,532 (169.7%) Food Services 1,803 1,861 ( 3.1%) (31) 54 (157.4%) Plant Maintenance & Operations 2,765 2,873 ( 3.8%) (2,695) 2,753 (197.9%) Debt Service Interest & Fiscal Charges ( 9.9%) (483) 536 (190.1%) The decrease in functional expenses is primarily due to adjustments to functional expenses to record the State's negative on-behalf contributions for OPEB in conjunction with the implementation of GASB 75. FINANCIAL ANALYSIS OF THE DISTRICT S FUNDS As noted earlier, Raymondville ISD uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. General Fund The fund balance of the Raymondville ISD s General Fund is $10,225,270 as of June 30, The 16.5% increase is a result of monitoring budgets and expenditures throughout the fiscal year and additional funding related to TRE. 9

25 MANAGEMENT S DISCUSSION AND ANALYSIS - CONTINUED General Fund Budgetary Highlights Differences between original & final budgets can be briefly summarized as follows: There was a change between the original and final budgets which reflects the use of fund balance for various board approved expenses. As we go through the year, budget amendments are being requested to move monies from one function to another which is consistent with the difference between original and final budgets. Differences between final budget and actual revenues and expenditures can be briefly summarized as follows: Revenues Increase in M&O tax collections as a result of a TRE election in September 2017 Increase in state aid as a result of TRE election Slight increase in enrollment Expenditures Various budget amendments were made during the year for various projects CAPITAL ASSETS AND DEBT ADMINISTRATION Capital Assets At the end of 2018, the District has invested in buildings and equipment, and vehicles in the amount of $244,815. The District also held an auction in which vehicles and equipment were sold. (See Table A-4.) More detailed information about the District s capital assets is presented in the notes to the financial statements. Table A-4 District s Capital Assets (In thousands of dollars) Governmental Activities Land $ 479 $ 479 Buildings and improvements 53,224 52,980 Furniture & Equipment 4,229 4,229 Vehicles 2,842 2,989 Capital Lease Assets Totals at historical cost 60,802 60,704 Total accumulated (26,551) (25,089) Net capital assets $ 34,251 $ 35,615 10

26 MANAGEMENT S DISCUSSION AND ANALYSIS - CONTINUED Long Term Debt At year-end the District had $16,046,057 outstanding as shown in Table A-5. Of this amount, $1,175,000 is due within the next year. More detailed information about the District s debt is presented in the notes to the financial statements. Table A-5 District s Long Term Debt (In thousands of dollars) Governmental Activities Bonds payable 15,605 16,710 Compensated absences Total long term debt 16,046 18,374 ECONOMIC FACTORS AND NEXT YEAR S BUDGETS AND RATES Appraised value used for the budget preparation is up $53,792,556 or 21% increase from last year. General operating fund spending per student increased in the budget from approximately $11,902 to $12,819, a 7.7% increase. The District s 2018 refined average daily attendance is expected to be 1,825. Additional commercial activity is expected to have a positive impact overall. These indicators were taken into account when adopting the general fund budget for Expenditures as budgeted are $21,961,792, an increase of 8.7% from actual expenditures. If these estimates are realized, the District s budgetary general fund balance is not expected to change depreciably by the close of CONTACTING THE DISTRICT S FINANCIAL MANAGEMENT This financial report is designed to provide citizens, taxpayers, customers, investors, and creditors with a general overview of the District s finances. If you have questions about this report or need additional financial information, contact the District s Business Office. 11

27

28 Data Control Codes STATEMENT OF NET POSITION JUNE 30, 2018 Primary Government Governmental Activities EXHIBIT A-1 ASSETS 1110 Cash and Cash Equivalents $ 1210 Property Taxes - Current 1220 Property Taxes Receivable (Delinquent) 1230 Allowance for Uncollectible Taxes 1240 Due from Other Governments 1267 Due from Fiduciary Funds 1290 Other Receivables, net 1410 Prepayments Capital Assets: 1510 Land 1520 Buildings, Net 1530 Furniture and Equipment, Net 1540 Other Capital Assets, Net 8,534, ,453 1,119,775 (122,823) 3,231, , , , ,351 30,498,010 2,021,455 1,252, Total Assets 48,435,301 DEFERRED OUTFLOWS OF RESOURCES 1705 Deferred Outflow Related to TRS Pension 1,304, Total Deferred Outflows of Resources 1,304,910 LIABILITIES 2110 Accounts Payable 2140 Interest Payable 2150 Payroll Deductions & Withholdings 2160 Accrued Wages Payable 2177 Due to Fiduciary Funds 2300 Unearned Revenue 2400 Payable from Restricted Assets Noncurrent Liabilities: 2501 Due Within One Year 2502 Due in More Than One Year 2540 Net Pension Liability (District's Share) 2545 Net OPEB Liability (District's Share 254, , ,457 1,635,435 61, ,999 2,250 1,616,472 15,573,118 5,251,258 11,768, Total Liabilities 37,089,443 DEFERRED INFLOWS OF RESOURCES 2605 Deferred Inflow Related to TRS Pension 6,288, Total Deferred Inflows of Resources 6,288,139 NET POSITION 3200 Net Investment in Capital Assets 3820 Restricted for Federal and State Programs 3850 Restricted for Debt Service 3860 Restricted for Capital Projects 3890 Restricted for Other Purposes 3900 Unrestricted 17,297, , ,745 1,377, ,000 (12,984,287) 3000 Total Net Position $ 6,362,628 The notes to the financial statements are an integral part of this statement. 12

29 Data Control Codes Primary Government: STATEMENT OF ACTIVITIES FOR THE YEAR ENDED JUNE 30, 2018 Program Revenues EXHIBIT B-1 Net (Expense) Revenue and Changes in Net Position Expenses Charges for Services Operating Grants and Contributions Primary Gov. Governmental Activities GOVERNMENTAL ACTIVITIES: Instruction $ 9,652,463 $ - $ 2,634,899 $ (7,017,564) Instructional Resources and Media Services 202, (202,141) Curriculum and Staff Development 571, ,006 (342,687) Instructional Leadership 334, ,235 (78,757) School Leadership 1,109,484-41,748 (1,067,736) Guidance, Counseling and Evaluation Services 803, ,660 (349,290) Social Work Services 145,343-82,441 (62,902) Health Services 169, ,269 (7,458) Student (Pupil) Transportation 385, (385,705) Food Services 1,803, ,962 1,643,182 (30,923) Extracurricular Activities 1,093,295 79,174 - (1,014,121) General Administration 1,018, ,230 5,833 (45,883) Facilities Maintenance and Operations 2,765,240 61,164 8,928 (2,695,148) Security and Monitoring Services 309, (309,804) Data Processing Services 193, (193,170) Community Services 51,774-49,346 (2,428) Debt Service - Interest on Long Term Debt 483, (483,345) Contracted Instructional Services Between Schools (284,291) ,291 Payments related to Shared Services Arrangements 191,553-55,169 (136,384) Other Intergovernmental Charges 99, (99,034) [TP] TOTAL PRIMARY GOVERNMENT: $ 21,100,435 $ 1,236,530 $ 5,623,715 (14,240,190) Data Control Codes MT DT SF GC IE MI TR General Revenues: Taxes: Property Taxes, Levied for General Purposes Property Taxes, Levied for Debt Service State Aid - Formula Grants Grants and Contributions not Restricted Investment Earnings Miscellaneous Local and Intermediate Revenue Total General Revenues 2,742, ,926 13,247,040 1,250, , ,860 18,235,554 CN Change in Net Position 3,995,364 NB PA NE Net Position - Beginning Prior Period Adjustment Net Position--Ending $ 23,026,139 (20,658,875) 6,362,628 The notes to the financial statements are an integral part of this statement. 13

30 BALANCE SHEET GOVERNMENTAL FUNDS JUNE 30, 2018 Data Control Codes 10 General Fund 211 ESEA Title 1 Part A 313 SSA-IDEA Part B ASSETS 1110 Cash and Cash Equivalents $ 7,948,772 $ - $ Property Taxes - Current 89, Property Taxes - Delinquent 899, Allowance for Uncollectible Taxes (Credit) (98,893) Receivables from Other Governments 1,794, , , Due from Other Funds 1,950, Other Receivables 157, Prepayments 314, Total Assets $ 13,054,925 $ 593,063 $ 517,495 LIABILITIES 2110 Accounts Payable $ 254,542 $ - $ Payroll Deductions and Withholdings Payable 135,084 17,358 14, Accrued Wages Payable 1,359, , , Due to Other Funds 188, , , Unearned Revenues Payable from Restricted Assets 2, Total Liabilities 1,939, , ,495 DEFERRED INFLOWS OF RESOURCES 2601 Unavailable Revenue - Property Taxes 890, Total Deferred Inflows of Resources 890, FUND BALANCES Restricted Fund Balance: 3450 Federal or State Funds Grant Restriction 3480 Retirement of Long-Term Debt Committed Fund Balance: 3510 Construction 3530 Capital Expenditures for Equipment 3600 Unassigned Fund Balance 302, ,000, , ,702, Total Fund Balances 10,225, Total Liabilities, Deferred Inflows & Fund Balances $ 13,054,924 $ 593,063 $ 517,495 The notes to the financial statements are an integral part of this statement. 14

31 EXHIBIT C-1 Other Funds Total Governmental Funds $ 585,341 $ 8,534,113 19, , ,998 1,119,775 (23,930) (122,823) 326,636 3,231, ,856 2,105, , ,308 $ 1,283,202 $ 15,448,685 $ - $ 254,542 5, ,457 27,222 1,635, ,846 1,326, , ,999-2, ,625 3,588, , , , , , ,656 1,377, , ,177 8,920, ,578 10,969,848 $ 1,283,203 $ 15,448,685 15

32 RECONCILIATION OF THE GOVERNMENTAL FUNDS BALANCE SHEET TO THE STATEMENT OF NET POSITION JUNE 30, 2018 Total Fund Balances - Governmental Funds 1 Capital assets used in governmental activities are not financial resources and therefore are not reported in governmental funds. At the beginning of the year, the cost of these assets was $60,704,495 and the accumulated depreciation was ($25,089,350). In addition, long-term liabilities, including bonds payable, are not due and payable in the current period, and, therefore are not reported as liabilities in the funds. The net effect of including the beginning balances for capital assets (net of depreciation) and long-term debt in the governmental activities is to decrease net position. Note: Beginning Balances related to TRS are NOT included in this amount. 2 Current year capital outlays and long-term debt principal payments are expenditures in the fund financial statements, but they should be shown as increases in capital assets and reductions in long-term debt in the government-wide financial statements. The net effect of including the 2017 capital outlays and debt principal payments is to decrease net position. 3 Included in the items related to debt is the recognition of the District's proportionate share of the net pension liability required by GASB 68. At the beginning of the year, the net position related to TRS was a Deferred Resource Outflow in the amount of $1,304,910, a Deferred Resource Inflow in the amount of $6,288,139 and a net pension liability in the amount of $6,351,247. Changes from the current year reporting of the TRS plan resulted in a decrease in net position in the amount of ($5,461,516). The combination of the beginning of the year amounts and the changes during the year resulted in a difference between the ending fund balance and the ending net position in the amount of ($5,212,964). 4 The 2018 depreciation expense increases accumulated depreciation. The net effect of the current year's depreciation is to decrease net position. $ EXHIBIT C-2 10,969,847 17,247, ,922 (5,461,516) (1,607,486) 5 The district implemented GASB 75 reporting requirements for the OPEB benefit plan through TRS. Since this is the first year of implementation, a prior period adjustment had to be made in the amount of ($20,658,875). The District's share of the TRS plan resulted in a net OPEB liability of ($11,768,028), a deferred outflow of $149,618 nd a deferred inflow of ($4,922,589). This resulted in a difference between the ending fund balance and the ending net of position. 6 Various other reclassifications and eliminations are necessary to convert from the modified accrual basis of accounting to accrual basis of accounting. These include recognizing unavailable revenue from property taxes as revenue, reclassifying the proceeds of bond sales as an increase in bonds payable, and recognizing the liabilities associated with maturing long-term debt and interest. The net effect of these reclassifications and recognitions is to increase net position. 19 Net Position of Governmental Activities $ (16,540,999) 890,036 6,362,628 The notes to the financial statements are an integral part of this statement. 16

33 STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCE GOVERNMENTAL FUNDS FOR THE YEAR ENDED JUNE 30, 2018 Data Control Codes 10 General Fund 211 ESEA Title 1 Part A 313 SSA-IDEA Part B REVENUES: Total Local and Intermediate Sources $ 4,422,391 $ - $ - State Program Revenues 17,030, Federal Program Revenues 2,098,168 1,251,293 1,471, Total Revenues 23,550,796 1,251,293 1,471,602 EXPENDITURES: Current: 0011 Instruction 0012 Instructional Resources and Media Services 0013 Curriculum and Instructional Staff Development 0021 Instructional Leadership 0023 School Leadership 0031 Guidance, Counseling and Evaluation Services 0032 Social Work Services 0033 Health Services 0034 Student (Pupil) Transportation 0035 Food Services 0036 Extracurricular Activities 0041 General Administration 0051 Facilities Maintenance and Operations 0052 Security and Monitoring Services 0053 Data Processing Services 0061 Community Services Debt Service: 0071 Principal on Long Term Debt 0072 Interest on Long Term Debt Capital Outlay: 0081 Facilities Acquisition and Construction Intergovernmental: 0093 Payments to Fiscal Agent/Member Districts of SSA 0099 Other Intergovernmental Charges 10,417, , , , ,582 51,914 94, ,527 70,565-1,433,206-36, , , , , , , ,876, ,241, ,191, ,922, , , ,068 14, , , , Total Expenditures 22,099,579 1,251,293 1,471, Net Change in Fund Balances 1,451, Fund Balance - July 1 (Beginning) 8,774, Fund Balance - June 30 (Ending) $ 10,225,270 $ - $ - The notes to the financial statements are an integral part of this statement. 17

34 EXHIBIT C-3 Other Funds Total Governmental Funds $ 553,362 $ 4,975,753 1,191,439 18,221, ,448 2,541,249 5,617,511 28,814, , , ,036 5,329 45,237 82,441 16, ,227 12, ,008 1,105, ,950-13,075, , , ,128 1,474,954 1,054, , , ,597 1,876,057 1,241,349 1,199,371 2,934, , ,437 55,413 1,105, ,950 65,567 77, ,553-99,034 3,099,833 27,922,307 (558,584) 892,633 1,303,161 10,077,214 $ 744,577 $ 10,969,847 18

35 EXHIBIT C-4 RECONCILIATION OF THE GOVERNMENTAL FUNDS STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES TO THE STATEMENT OF ACTIVITIES FOR THE YEAR ENDED JUNE 30, 2018 Total Net Change in Fund Balances - Governmental Funds Current year capital outlays and long-term debt principal payments are expenditures in the fund financial statements, but they should be shown as increases in capital assets and reductions in long-term debt in the government-wide financial statements. The net effect of removing the 2017 capital outlays and debt principal payments is to decrease net position. Depreciation is not recognized as an expense in governmental funds since it does not require the use of current financial resources. The net effect of the current year's depreciation is to decrease net position. $ 892,633 1,460,872 (1,607,486) Various other reclassifications and eliminations are necessary to convert from the modified accrual basis of accounting to accrual basis of accounting. These include recognizing unavailable revenue from property taxes as revenue, adjusting current year revenue to show the revenue earned from the current year's tax levy, reclassifying the proceeds of bond sales, and recognizing the liabilities associated with maturing long-term debt and interest. The net effect of these reclassifications and recognitions is to decrease net position. 931,393 Current year changes due to GASB 68 decreased revenues in the amount of $252,308 but also increased expenditures in the amount of $1,547,616. The net effect on the change in the ending net position was a decrease in the amount of $1,799,924. (1,799,924) The implementation of GASB 75 to report the District's share of the TRS OPEB plan resulted in a prior period adjustment of ($20,658,875). The changes in the ending net position as a result of reporting the OPEB items was a increased in the change in net position in the amount of $4,117,876. Change in Net Position of Governmental Activities $ 4,117,876 3,995,364 The notes to the financial statements are an integral part of this statement. 19

36 STATEMENT OF FIDUCIARY NET POSITION FIDUCIARY FUNDS JUNE 30, 2018 EXHIBIT E-1 Agency Funds ASSETS Cash and Cash Equivalents $ Due from Other Funds 864,191 61,809 Total Assets $ 926,000 LIABILITIES Accounts Payable $ Payroll Deductions and Withholdings Payable Accrued Wages Payable Due to Other Funds Due to Student Groups 1,132 3,179 16, ,558 63,883 Total Liabilities $ 926,000 The notes to the financial statements are an integral part of this statement. 20

37

38 NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2018 I. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (the "District") is a public educational agency operating under the applicable laws and regulations of the State of Texas. It is governed by a seven-member Board of Trustees (the "Board") elected by registered voters of the District. The District prepares its basic financial statements in conformity with generally accepted accounting principles (GAAP) promulgated by the Governmental Accounting Standards Board (GASB) and other authoritative sources identified in GASB Statement No. 76, and it complies with the requirements of the appropriate version of Texas Education Agency's Financial Accountability System Resource Guide (the "Resource Guide") and the requirements of contracts and grants of agencies from which it receives funds. Pensions. The fiduciary net position of the Teacher Retirement System of Texas (TRS) has been determined using the flow of economic resources measurement focus and full accrual basis of accounting. This includes for purposes of measuring the net pension liability, deferred outflows of resources and deferred inflows of resources related to pensions, pension expense, and information about assets, liabilities and additions to/deductions from TRS's fiduciary net position. Benefit payments (including refunds of employee contributions) are recognized when due and payable in accordance with the benefit terms. Investments are reported at fair value. Other Post-Employment Benefits. The fiduciary net position of the Teacher Retirement System of Texas (TRS) TRS Care Plan has been determined using the flow of economic resources measurement focus and full accrual basis of accounting. This includes for purposes of measuring the net OPEB liability, deferred outflows of resources and deferred inflows of resources related to other post-employment benefits, OPEB expense, and information about assets, liabilities and additions to/deductions from TRS Care s fiduciary net position. Benefit payments are recognized when due and payable in accordance with the benefit terms. There are no investments as this is a pay-as you-go plan and all cash is held in a cash account. applies Governmental Accounting Standards Board ("GASB") Statement No. 72, Fair Value Measurement and Application. GASB Statement No. 72 provides guidance for determining a fair value measurement for reporting purposes and applying fair value to certain investments and disclosures related to all fair value measurements. A. REPORTING ENTITY The Board of Trustees (the "Board") is elected by the public and it has the authority to make decisions, appoint administrators and managers, and significantly influence operations. It also has the primary accountability for fiscal matters. Therefore, the District is a financial reporting entity as defined by the Governmental Accounting Standards Board ("GASB") in its Statement No. 14, "The Financial Reporting Entity. There are no component units included within the reporting entity. 21

39 NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2018 I. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) B. GOVERNMENT-WIDE AND FUND FINANCIAL STATEMENTS The Statement of Net Position and the Statement of Activities are government-wide financial statements. They report information on all of the RAYMONDVILLE INDEPENDENT SCHOOL DISTRICT nonfiduciary activities with most of the interfund activities removed. Governmental activities include programs supported primarily by taxes, State foundation funds, grants and other intergovernmental revenues. Business-type activities include operations that rely to a significant extent on fees and charges for support. The Statement of Activities demonstrates how other people or entities that participate in programs the District operates have shared in the payment of the direct costs. The "charges for services" column includes payments made by parties that purchase, use, or directly benefit from goods or services provided by a given function or segment of the District. Examples include tuition paid by students not residing in the district, school lunch charges, etc. The "grants and contributions" column includes amounts paid by organizations outside the District to help meet the operational or capital requirements of a given function. Examples include grants under the Elementary and Secondary Education Act. If a revenue is not a program revenue, it is a general revenue used to support all of the District's functions. Taxes are always general revenues. Interfund activities between governmental funds appear as due to/due froms on the Governmental Fund Balance Sheet and as other resources and other uses on the governmental fund Statement of Revenues, Expenditures and Changes in Fund Balance. All interfund transactions between governmental funds are eliminated on the government-wide statements. Interfund activities between governmental funds and fiduciary funds remain as due to/due from on the government-wide Statement of Activities. The fund financial statements provide reports on the financial condition and results of operations for three fund categories - governmental, proprietary, and fiduciary. Since the resources in the fiduciary funds cannot be used for District operations, they are not included in the government-wide statements. The District considers some governmental funds major and reports their financial condition and results of operations in a separate column. Proprietary funds distinguish operating revenues and expenses from nonoperating items. Operating revenues result from providing goods and services in connection with a proprietary fund's principal ongoing operations; they usually come from exchange or exchange-like transactions. All other revenues are nonoperating. Operating expenses can be tied specifically to the production of the goods and services, such as materials and labor and direct overhead. Other expenses are nonoperating. C. MEASUREMENT FOCUS, BASIS OF ACCOUNTING, AND FINANCIAL STATEMENT PRESENTATION The government-wide financial statements use the economic resources measurement focus and the accrual basis of accounting. Revenues are recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of the related cash flows. Property taxes are recognized as revenues in the year for which they are levied. Grants and similar items are recognized as revenue as soon as all eligibility requirements imposed by the provider have been met. 22

40 NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2018 I. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) C. MEASUREMENT FOCUS, BASIS OF ACCOUNTING, AND FINANCIAL STATEMENT PRESENTATION (CONTINUED) Governmental fund financial statements use the current financial resources measurement focus and the modified accrual basis of accounting. With this measurement focus, only current assets, current liabilities and fund balances are included on the balance sheet. Operating statements of these funds present net increases and decreases in current assets (i.e., revenues and other financing sources and expenditures and other financing uses). The modified accrual basis of accounting recognizes revenues in the accounting period in which they become both measurable and available, and it recognizes expenditures in the accounting period in which the fund liability is incurred, if measurable, except for unmatured interest and principal on long-term debt, which is recognized when due. The expenditures related to certain compensated absences and claims, and judgments are recognized when the obligations are expected to be liquidated with expendable available financial resources. The District considers all revenues available if they are collectible within 60 days after year end. Revenues from local sources consist primarily of property taxes. Property tax revenues and revenues received from the State are recognized under the "susceptible to accrual" concept, that is, when they are both measurable and available. The District considers them "available" if they will be collected within 60 days of the end of the fiscal year. Miscellaneous revenues are recorded as revenue when received in cash because they are generally not measurable until actually received. Investment earnings are recorded as earned, since they are both measurable and available. Grant funds are considered to be earned to the extent of expenditures made under the provisions of the grant. Accordingly, when such funds are received, they are recorded as unearned revenues until related and authorized expenditures have been made. If balances have not been expended by the end of the project period, grantors sometimes require the District to refund all or part of the unused amount. The Fiduciary Funds are accounted for on a flow of economic resources measurement focus and utilize the accrual basis of accounting. This basis of accounting recognizes revenues in the accounting period in which they are earned and become measurable and expenses in the accounting period in which they are incurred and become measurable. With this measurement focus, all assets and all liabilities associated with the operation of these funds are included on the fund Statement of Net Position. The fund equity is segregated into invested in capital assets net of related debt, restricted net assets, and unrestricted net assets. Agency Funds utilize the accrual basis of accounting but do not have a measurement focus as they report only assets and liabilities. 23

41 NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2018 I. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) D. FUND ACCOUNTING The District reports the following major governmental funds: 1. The General Fund The general fund is the District's primary operating fund. It accounts for all financial resources except those required to be accounted for in another fund. ESEA, Title 1, Part A Improving Basic Programs (211). To account for funds allocated to allocated to the District to enable the District to provide opportunities for children served to acquire the knowledge and skills contained in the challenging State content standards and to meet the challenging State performance standards developed for all children. SSA, IDEA Part B, Formula (224). To account for funds granted to operate education programs for children with disabilities. Additionally, the District reports the following fund type(s): Governmental Funds: 1. Special Revenue Funds The District accounts for resources restricted to, or designated for, specific purposes by the District or a grantor in a special revenue fund. Most Federal and some State financial assistance is accounted for in a Special Revenue Fund, and sometimes unused balances must be returned to the grantor at the close of specified project periods. 2. Debt Service Funds The District accounts for resources accumulated and payments made for principal and interest on long-term general obligation debt of governmental funds in a debt service fund. 3. Capital Projects Funds The proceeds from long-term debt financing and revenues and expenditures related to authorized construction and other capital asset acquisitions are accounted for in a capital projects fund. Fiduciary Funds: 1. Agency Funds The District uses these funds to report student activity funds and other resources held in a purely custodial capacity (assets equal liabilities). Agency funds typically involve only the receipt, temporary investment and remittance of the fiduciary resources to individuals, private organizations, or other governments. E. OTHER ACCOUNTING POLICIES 1. Property taxes are levied by October 1 on the assessed value listed as of the prior January 1 for all real and business personal property in conformance with Subtitle E, Texas Property Tax Code. Taxes are due on receipt of the tax bill and are delinquent if not paid before February 1 of the year following the year in which imposed. On January 1 of each year, a tax lien attaches to property to secure the payment of all taxes, penalties, and interest ultimately imposed. Property tax revenues are considered available (1) when they become due or past due and receivable within the current period and (2) when they are expected to be collected during a 60-day period after the close of the fiscal year. 24

42 NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2018 I. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) E. OTHER ACCOUNTING POLICIES (CONTINUED) 2. Allowances for uncollectible tax receivables within the General and Debt Service Funds are based upon historical experience in collecting property taxes. Uncollectible personal property taxes are periodically reviewed and written off, but the District is prohibited from writing off real property taxes without specific statutory authority from the Texas Legislature. 3. The District uses the purchase method of accounting for inventory. An immediate change for inventory costs is recorded under the appropriate supply expenditure code and inventories are not reported on the balance sheet unless there is a significant amount at the fiscal year end. There were not significant amounts of inventory on hand at June 30, Capital assets, which include land, buildings, furniture and equipment [and infrastructure assets] are reported in the applicable governmental or business-type activities columns in the government-wide financial statements. Capital assets are defined by the District as assets with an initial, individual cost of more than $5,000 and an estimated useful life in excess of two years. Such assets are recorded at historical cost or estimated historical cost if purchased or constructed. Donated capital assets are recorded at estimated fair market value at the date of donation. The costs of normal maintenance and repairs that do not add to the value of the asset or materially extend assets lives are not capitalized. Major outlays for capital assets and improvements are capitalized as projects are constructed. Buildings, furniture and equipment of the District [and the component units] are depreciated using the straight-line method over the following estimated useful lives: Asset Class Estimated Useful Lives Buildings & Improvements Vehicles 7 Furniture and Equipment Long-term Obligations, in the government-wide financial statements, and proprietary fund types in the fund financial statements, long-term debt and other long-term obligations are reported as liabilities in the applicable governmental activities, business-type activities, or proprietary fund type statement of net assets. Bond premiums and discounts are deferred and amortized over the life of the bonds using the effective interest method. Bonds payable are reported net of the applicable bond premium or discount. In the fund financial statements, governmental fund types recognize bond premiums and discounts, as well as bond issuance costs, during the current period. The face amount of debt issued is reported as other financing sources. Premiums received on debt issuances are reported as other financing sources while discounts on debt issuances are reported as other financing uses. Issuance costs, whether or not withheld from the actual debt proceeds received, are reported as debt service expenditures. 25

43 NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2018 I. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) E. OTHER ACCOUNTING POLICIES (CONTINUED) 6. It is the District's policy to permit some employees to accumulate earned but unused vacation and sick pay benefits. There is no liability for unpaid accumulated sick leave since the District does not have a policy to pay any amounts when employees separate from service with the district. All vacation pay is accrued when incurred in the government-wide, proprietary, and fiduciary fund financial statements. A liability for these amounts is reported in governmental funds only if they have matured, for example, as a result of employee resignations and retirements. 7. When the District incurs an expense for which it may use either restricted or unrestricted assets, it uses the restricted assets first unless unrestricted assets will have to be returned because they were not used 8. In the fund financial statements, governmental funds report fund balance as nonspendable if the amounts cannot be spent because they are either not in spendable form or are legally or contractually required to remain intact. Restrictions of fund balance are for amounts that are restricted to specific purposes by an external entity (creditors, grantors, governmental regulations) or the restriction is imposed by law through constitutional provision or enabling legislation. Commitments of fund balance represent amounts that can only be used for specific purposes pursuant to constraints imposed by the District's Board. Assignments of fund balance are amounts set aside by the District's Superintendent or his designee with the intent they be used for specific purposes. 9. When the District incurs an expense for which it may use either restricted or unrestricted assets, it uses the restricted assets first whenever they will have to be returned if they are not used 10. The District reports investments at fair value for reporting purposes. 11. Deferred outflows of resources, in addition to assets, the statement of financial position will sometimes report a separate section for deferred outflows of resources. This separate financial statement element, deferred outflows of resources related to the TRS pension plan, represents a consumption of net position that applies to a future period(s) and so will not be recognized as an outflow of resources. 12. Deferred inflows of resources, in addition to liabilities, the statement of financial position will sometimes report a separate section for deferred inflows of resources. This separate financial statement element, deferred inflows of resources, represents an acquisition of net position that applies to a future period(s) and so will not be recognized as an inflow of resources (revenue) until that time. The District has one type of item which arises only under a modified accrual basis of accounting that qualifies for reporting in this category. Uncollected property taxes which are assumed collectible are reported in this category on the balance sheet for governmental funds. They are not reported in this category on the government wide statement of net position. 13. The Data Control Codes refer to the account code structure prescribed by TEA in the Financial Accountability System Resource Guide. Texas Education Agency requires school districts to display these codes in the financial statements filed with the Agency in order to insure accuracy in building a Statewide data base for policy development and funding plans. 26