Suhdannenäkymät tyyntä myrskyn edessä?

|

|

|

- Annemari Eeva-Kaarina Hovinen

- 9 vuotta sitten

- Katselukertoja:

Transkriptio

1 Macro Research 7 April, 2011 Suhdannenäkymät tyyntä myrskyn edessä? Maaliskuu 2011 Tiina Helenius Pääekonomisti, Suomi Handelsbanken Capital Markets

2 Talouskasvu ja talouspolitiikka dominoivat kriiseistä huolimatta 2

3 Punainen lanka Maailmantalouden elpyminen finanssikriisin jälkeisestä laskusuhdanteesta on edennyt siihen pisteeseen, että kehittyvät taloudet ylikuumenevat, jos ne eivät hillitse talouskasvuaan. Ovatko ne jo myöhästyneet, kun inflaatio kiihtyy? Länsimaat (G3) eivät ole vielä entisenlaisen kysynnän y tasolla, työttömyysasteet yy ovat edelleen korkealla tasolla. Kallistunut energia uhkaa kaventaa ostovoimaa ja kutistaa yritysmarginaaleja. Miten keskuspankin reagoivat tuontina saatuihin inflaatiopaineisiin? JA TÄHÄN PÄÄLLE KRIISIT Euroalueen velkakriisi k i selviääkö Espanja omin neuvoin? Geopoliittinen kriisi Pohjois-Afrikassa ja Lähi-Idässä miksi juuri nyt ja mitä vaikutuksia sillä on maailmantalouteen? Japani uhkaako maailmantalouden kasvua 3

4 Öljy on kasvuriski 1. öljykriisi 2. öljykriisi Persianlahden sota Irak 4

5 MENA: lähi-ajan uhka, pitkän ajan mahdollisuus paljon vihaisia ja köyhiä nuoria, jotka valjastaa työvoimaan! BKT/henkilö Väestön määrä Alle 30 vuotiaita US dollaria milj. %:a väestöstä Algeria Bahrain Egypti Jordania Kuwait Libanon Libya Marokko Oman Qatar Saudi Arabia Tunisia Arabiemiirikunnat Lähde: IMF & Standard Chartered Research 5

6 Kehittyvät taloudet raaka-aineiden kallistumisen takana 650 Raaka-ainehinnat (CRB, Raw Industrials) Percent Index Source: Reuters EcoWin 6

7 Kehittyvät markkinat kompensoivat lännen heikkoa kysyntää Automarkkinat EM vs. DM: osuudet, %:a yhteenlasketusta myynnistä 7

8 USA suuntautunut viennissään kehittyville markkinoille 8

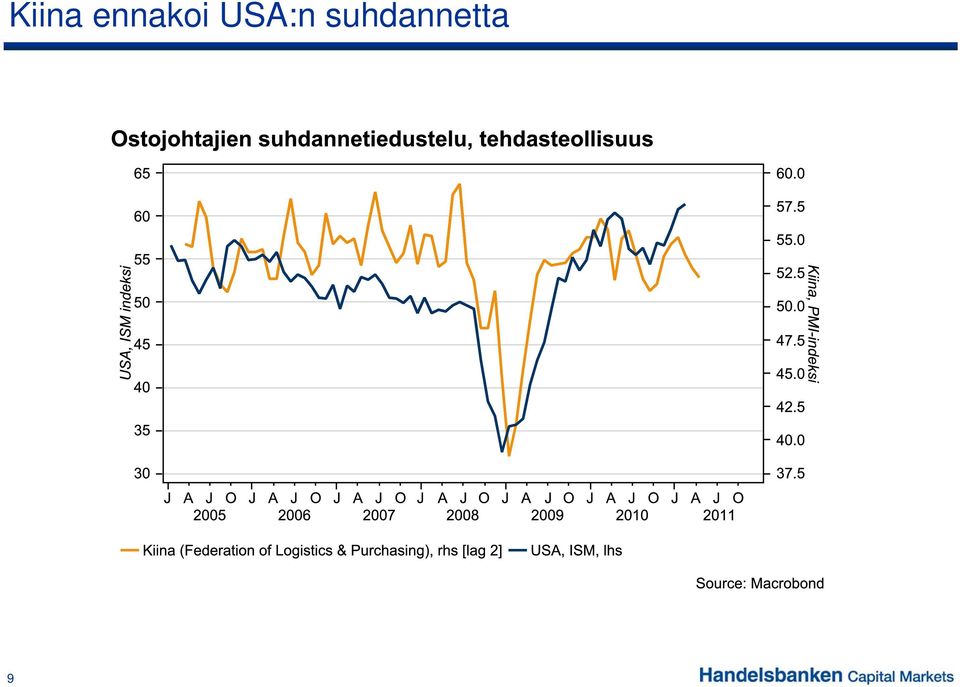

9 Kiina ennakoi USA:n suhdannetta 9

10 Kiina haluaa kasvaa hitaammin Luotonanto t yksityiselle i sektorille (pl. rahoitussektori) i) Vuos simuutos, % USA Kiina EMU Source: Reuters EcoWin 10

11 Kiinan katseet ehdottomasti inflaatiossa Seuraa luottosykliä! 11

12 Aasia jäälleen vauhdissa pienen suvantovaiheen jälkeen Tuonti (vol.), 07/2008= In ndex LatAm Aasia USA EMU Itä-Eurooppa & Venäjä 70 Jul Nov Mar Jul Nov Mar Jul Nov Mar Jul Source: Reuters EcoWin 12

13 Kallis öljy vauhdittaa Venäjää USD (billions) USD D/barreli Source: Reuters EcoWin 13

14 Saksan teollisuus supervahva etelän velkakriisistä huolimatta Toimintaympäristö, nykytila Odotukset (seuraavat 6 kk) 100 Indeksi IFO--indeksi Source: Reuters EcoWin

15 Euroalue ei juuri auta Saksaa Index 15

16 vaan Saksa noussut kehittyvien talouksien avulla! 9 8 EUR (b billions) USA BRIC Source: Reuters EcoWin 16

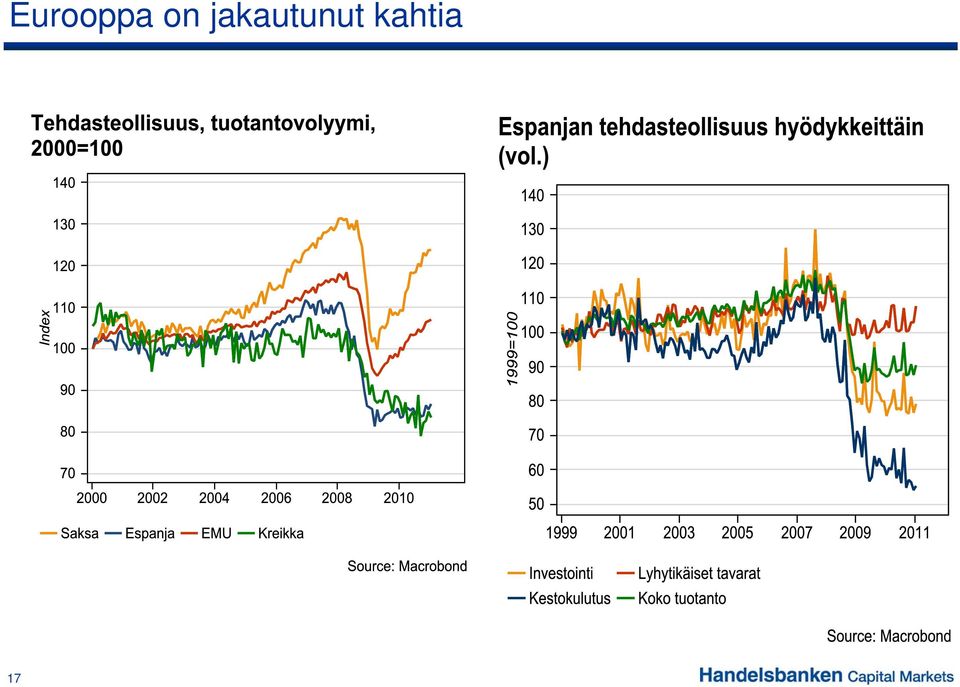

17 Eurooppa on jakautunut kahtia 17

18 Suuria eroja erikoistumisessa pääomahyödykkeet nostavat Saksaa Investointihyödykkeiden vientitilaukset (vol.) Saksa 2001= = Ruotsi EMU Espanja Source: Reuters EcoWin 18

19 Suomi kuuluu Saksan leiriin! 19

20 Hyvät, pahat ja rumat Rakennussektori suhteessa talouteen edelleen liian suuri Espanjassa? 20

21 Espanjalainen kuluttaja putoaaaaaaaaaaaaaaaa 21

22 Onko siis takeita kasvusta? 22

23 Riskin uudelleenhinnoittelu pysyvää, jos tilanne ei parane 23

24 Julkisen talouden kutistus vasta alullaan Miljardia EUR, 12 kk:n vuosisumma 24

25 Espanja ei leikkaa tarpeeksi Lähde: IMF Fiscal Monitor Nov

26 Julkinen velka on vain jäävuoren huippu Yksityisen sektorin velka, %:a BKT:sta Irlanti Espanja Portugali EMU Italia Kreikka 26

27 Heikkojen pankkien rahoituskustannukset kestämättömät Caja de Ahorros y Monte de Piedad de Madrid Banco Espirito Santo Caixa General de depositos BBVSM Santander Handelsbanken 27

28 Rahapolitiikka 28

29 Inflaatiopaineet reaalitaloudesta: länsi vs. kehittyvät taloudet Index Tilaa kasvaa puku ratkeaa! 29

30 Euroalue: rahoituksen välitysmekanismi epäkunnossa? Markkinat hinnoittelevat useita koronnostoja seuraavalle 12 kk:lle 30

31 EKP lähempänä neutraalia korkoa kuin USA:n keskuspankki 31

32 Aggressiivinen EKP => vahvistaa euroa ja hillitsee samalla energiasta ja raaka-aineista peräisin olevia inflaatiopaineita 32

33 Suomi kiilaa jälleen, kestääkö se? 33

34 Suomelle korkotaso on tarpeettoman elvyttävä 34

35 ja korko vauhdittaa Suomen asuntomarkkinoita Asuntojen hinnat Suomessa, 1995/01= Nimellishinnat KHI-deflatoitu Ansiotasolla deflatoitu Source: Reuters EcoWin 35

36 Kotimainen kulutuskysyntä entisellään Suomessa USA UK Saksa Suomi Japani EMU Source: Reuters EcoWin 36

37 Handelsbankenin Suomen talousennuste (joulukuu 2010) Suomen kasvuennusteet, % Prosenttimuutos, s suluissa edellinen ennuste E 2011E 2012E Yksityinen kulutus 1.7-1,9 2,7 (2,6) 2,5 (2,4) 2,4 (2,3) Julkinen kulutus 2.4 1,2 0,5 (0,5) 0,5 (0,5) 0,5 (0,5) Investoinnit ,7 1,9 (0,9) 6,5 (5,3) 5,4 (5,6) Vienti ,3 5,9 (11,0) 5,4 (5,8) 6,8 (6,6) Tuo nti ,1 2,6 (8,0) 5,5 (5,7 ) 5,1 (5,6) B KT 0.9-8,0 3,4 (3,4) 2,9 (2,7) 3,2 (3,0) A nsio taso indeksi 5.5 4,0 2, Kuluttajahintaindeksi Teo llisuustuo tanto Työ ttö myysaste* Julkisyhteisö jen raho itusjäämä** * prosenttia työvoimasta ** prosenttia BKT:sta Lähde: Handelsbanken 37

38 Keskeiset BKT:n konsensusennusteet Lähde: Consensus Economics, Feb 2011 Survey 38

39 Maailmantalouden BKT-osuudet Ostovoimakorjatut osuudet Other 28% PPP GDP in 2009 (IMF) EU 21% Osuudet nykyrahassa (USD) Other 23% Nominal GDP 2009 (IMF) EU 28% 39 Brazil Russia 3% US 21% Brazil 3% Russia 2% 3% India 2% India 5% China 13% Japan 6% Ostovoimakorjattu BKT huomioi eri maiden väliset erot hintatasossa. Hintataso on tyypillisesti matalampi kehittyvissä maissa, mikä tarkoittaa, että reaalitulot ovat korkeammat, mitä nimellistulot indikoivat. China 8% Japan 9% US 25% Vaikka BRIC-maiden osuus maailmantaloudesta on pienempi nykydollareissa kuin ostovoimakorjattuna, alueen absoluuttinen kasvu nykydollareissa on suurempi kuin USA:n.

40 Disclaimer Research Disclaimers Handelsbanken Capital Markets, a division of Svenska Handelsbanken AB (publ) (collectively referred to herein as SHB ) is responsible for the preparation of this research report. All research reports are prepared in accordance with the recommendations of the Swedish, Finnish, Danish and Norwegian Securities Dealers Associations and are based on data collected from trade and statistical services and other information sources which SHB considers to be reliable. SHB does not represent that such information is true, accurate or complete and it should not be relied upon as such. In no event will SHB or any of its affiliates, their officers, directors or employees be liable to any person for any direct, indirect, special or consequential damages arising out of any use of the information contained in the research reports, including without limitation any lost profits even if SHB is expressly advised of the possibility or likelihood of such damages. No independent verification exercise has been undertaken in respect of this information. This research report may have been presented to the subject company for factual content verification before publication. The recommendation has not been changed as a consequence of such factual verification. Any opinions expressed are the opinions of employees of SHB and its affiliates and reflect their judgment at this date and are subject to change. The information in the research reports does not constitute a personal recommendation or investment advice. Reliance should not be placed on reviews or opinions expressed when taking investment or strategic decisions. SHB, its affiliates, their clients, officers, directors or employees own or have positions in securities mentioned in research reports. SHB and/or its affiliates provide investment banking and non-investment banking financial services, including corporate banking services; and, securities advice to issuers of securities mentioned in research reports. This document does not constitute or form part of any offer for sale or subscription of or solicitation of any offer to buy or subscribe for any securities nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever. Past performance may not be repeated and should not be seen as an indication of future performance. The value of investments and the income from them may go down as well as up and investors may forfeit all principal originally invested. Investors are not guaranteed to make profits on investments and may lose money. Exchange rates may cause the value of overseas investments and the income arising from them to rise or fall. This research product will be updated on a regular basis. The distribution of this document in certain jurisdictions may be restricted by law and persons into whose possession this document comes should inform themselves about, and observe, any such restrictions. No part of SHB research reports may be reproduced or distributed to any other person without the prior written consent of SHB. Research reports are distributed in the UK by SHB. SHB is authorised by the Swedish Financial Supervisory Authority (Finansinspektionen), and regulated by the Financial Services Authority for the conduct of UK business. In the United Kingdom, the research reports are directed only at intermediate customers and market counterparties (as defined in the rules of the FSA) and the investments or services to which they relate are available only to such persons. The research reports must not be relied upon or acted on by private customers. UK customers should note that SHB does not participate in the UK Financial Services Compensation Scheme and UK customers will not be protected by that scheme. This does not exclude or restrict any duty or liability that SHB has to its customers under the regulatory system in the United Kingdom. Handelsbanken Capital Markets has established procedures to prevent conflicts of interest and to ensure that all research is presented based on objectivity and independence. The ethical standards are documented in Guidelines for Handelsbanken Capital Markets. Handelsbanken Capital Markets research departments are organised separately from and do not report to other business areas within the SHB sphere. SHB employees, including analysts, receive compensation that is generated by overall firm profitability. The views contained in SHB research reports accurately reflect the personal views of the respective analysts, and no part of analysts compensation is directly or indirectly related to specific recommendations or views expressed within research reports. For specific analyst certification, please contact Robert Gärtner In the United Kingdom Handelsbanken is regulated by the FSA but recipients should note that neither the UK Financial Services Compensation Scheme not the rules of the FSA made under the UK Financial Services and Markets Act 2000 for the protection of private customers apply to this research report. When distributed in the United States Important Third-Party Research Disclosures: Research reports are prepared by SHB for information purposes only. SHB and its employees are not subject to the NASD s research analyst conflict rules. SHB research reports are intended for distribution in the United States solely to major U.S. institutional investors, as defined in Rule 15a-6 under the Securities Exchange Act of Each major U.S. institutional investor that receives a copy of research report by its acceptance hereof represents and agrees that it shall not distribute or provide research reports to any other person. Reports regarding fixed-income products are prepared by SHB and distributed by SHB to major U.S. institutional investors under Rule 15a-6(a)(2). Any U.S. person receiving these research reports that desires to effect transactions in any fixed-income product discussed within the research reports should call or write SHB. Reports regarding equity products are prepared by SHB and distributed in the United States by Handelsbanken Markets Securities Inc. ( HMSI ) under Rule 15a-6(a)(2). Any U.S. person receiving these research reports that desires to effect transactions in any equity product discussed within the research reports should call or write HMSI. Please be advised of the following important research disclosure statements: Affiliates of HMSI (including SHB) expects to receive or intends to seek compensation for investment banking services from the subject company in the next three months; HMSI is a NASD Member, telephone number ( ). 40